The people's voice of reason

The people's voice of reason

Reciprocal tariffs are back, rates are back to 2024 levels — for now — and more.

Last week, global trade policy was dominated by sharp escalation in U.S. tariffs under the Trump administration. On July 31, a sweeping executive order set new reciprocal tariffs, ranging from 15 % baseline to as high as 50% on imports from countries like Canada, Brazil, India, Taiwan, and Switzerland, scheduled to take effect Aug. 7. These measures rattled global markets, with stock indices dropping and investor confidence wavering. India was singled out in U.S. policy rhetoric and tariff enforcement, with no exemptions granted, Freight Right Global Logistics reports. In response, the EU froze planned retaliatory tariffs for six months, signaling a temporary de-escalation and opening space for fresh negotiations. Amid this turbulence, the IMF reported that although global tariffs eased slightly in June, uncertainty remained elevated and trade policy unpredictability persisted globally.

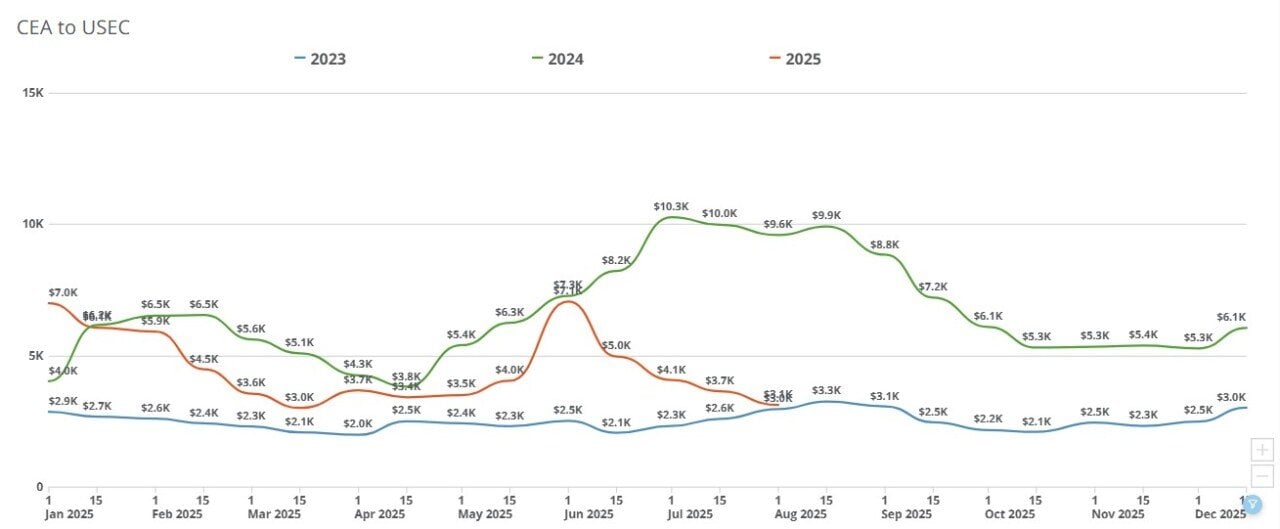

Transpacific ocean rates held largely steady this past week. China-U.S. West Coast (CEA-USWC) rates were unchanged at approximately $1,800-$2,342 per forty-foot equivalent unit (FEU), continuing three weeks of stability after the sharp post-June declines. China-U.S. East Coast (CEA-USEC) prices fell 4% to $3,100-$3,950/FEU, marking the sixth straight week of declines. Daily rates have continued easing slightly since the latest tariff-related executive order went into effect on Aug. 1.

TrueFreight Index (TFX) is reporting the following at-cost rates for the following container sizes this week. Graphics below illustrate specifically at-cost FEU rate trends.

Week of August 4, 2025:

The outlook for August remains bearish. Volumes are expected to stay flat or dip further, while forwarders continue to face compressed margins. A possible 90-day extension of the current 30% tariff rate on Chinese goods could trigger a brief spike in bookings, but any surge would likely be short-lived given earlier frontloading and cautious importer behavior. A possible general rate increase (GRI) could take place midway through August to return carriers to around break-even.

If no extension is granted and tariffs rise after Aug. 12, further disruption and delays in demand recovery are likely. With carriers already operating near break-even levels and importers reluctant to commit, the remainder of peak season appears muted, and rates are expected to hover near current levels unless a major policy shift jolts the market.

For additional resources regarding the Trump administration’s latest reciprocal tariff guidance, please refer to the administration’s latest Executive Order, Annex 1 of the Executive Order, Annex 2 of the Executive Order and US Customs & Border Protection guidance on Aug. 7 reciprocal tariffs.

This story was produced by Freight Right Global Logistics and reviewed and distributed by Stacker.

Reader Comments(0)