The people's voice of reason

The people's voice of reason

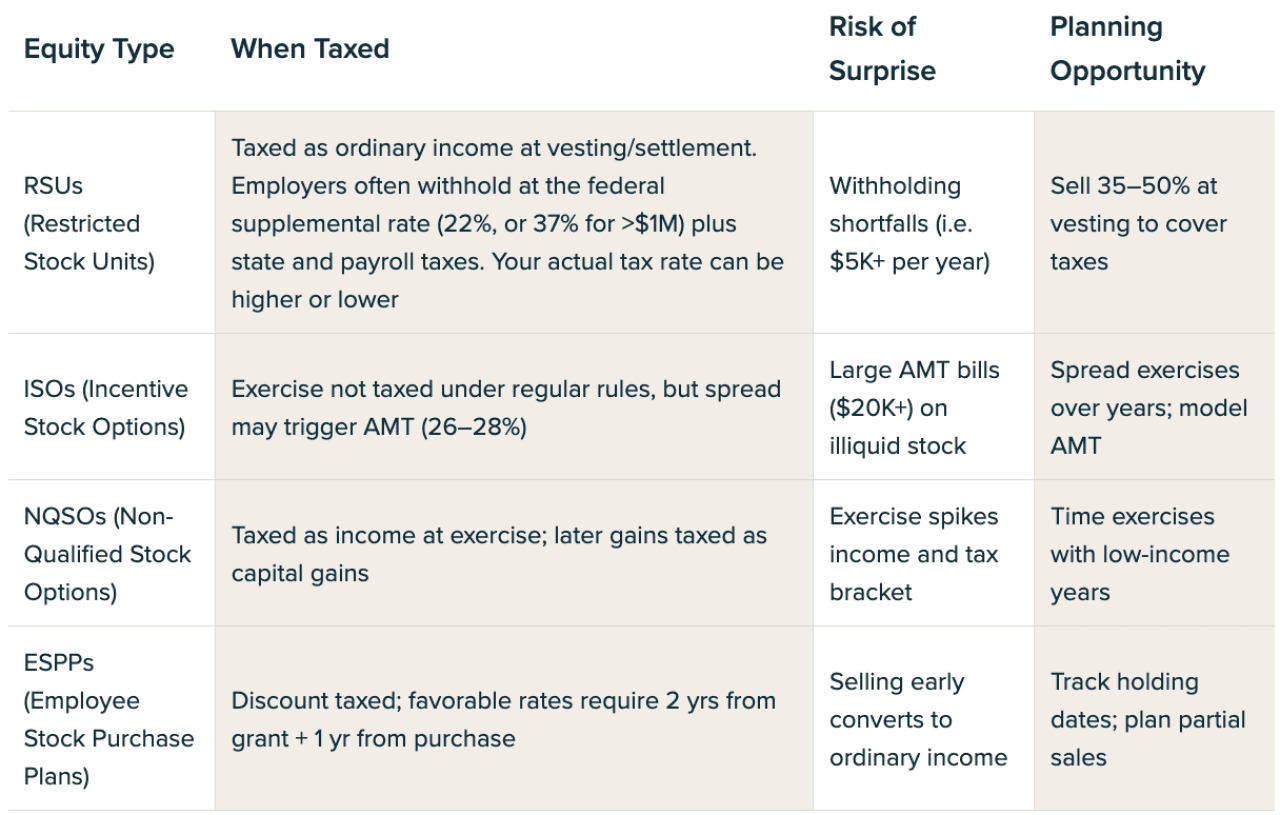

Equity compensation taxes often surprise tech professionals because company withholding rarely covers the full bill. Restricted stock units (RSUs) are taxed as income at vesting (not sale), incentive stock options (ISOs) can trigger alternative minimum tax (AMT), employee stock purchase plan (ESPP) shares lose benefits if sold too soon, and moving states midvesting can create unexpected liabilities. To avoid traps, Domain Money recommends calculating your true tax rate, selling systematically to cover obligations, and coordinating with a certified financial planner and tax professional to manage timing, diversification, and cash flow.

For some tech employees, equity compensation can make up 30%-70% of total income. Mismanaging the tax rules can easily cost five or even six figures in surprise bills, penalties, or missed opportunities. With proper planning, you can turn equity into long-term, tax-efficient wealth.

1. Believing RSUs Are Taxed at Sale

The trap: Many think RSUs are like regular stock. They’re not. Taxes hit at vesting, even if you don’t sell.

Example: Marcus in California vested $80,000 in RSUs. Withholding covered around 28%, but his true rate was 35%. Result: a $5,400 bill at filing.

Fix:

2. Panic-Selling Everything at Vesting

The trap: After learning taxes hit at vesting, some sell 100% immediately.

Example: Sarah sold $120,000 of RSUs in one year, pushing her into the 32% bracket and costing an extra $6,400 in taxes.

Fix:

3. ISO Exercises That Trigger AMT

The trap: ISOs feel tax-free at exercise — until AMT hits.

Example: David exercised ISOs with a $150,000 spread. Regular tax: $0. AMT owed: $42,000 on illiquid stock.

Fix:

4. Wash Sale Rule Violations

The trap: Selling stock at a loss while new RSUs or ESPP shares arrive can void your tax benefit. Check your vesting calendar before loss harvesting company stock. If bonus/award shares (including RSUs when delivered) arrive within 30 days, wash-sale rules can disallow the loss — even if your broker doesn’t report it automatically.

Example: Jennifer harvested a $10,000 loss, but new RSUs vested within 30 days. Loss was disallowed.

Fix:

5. Multistate Tax Complications

The trap: Moving states doesn’t always free you from old obligations.

Example: Alex worked in California (13.3% tax), then moved to Texas. California still taxed equity linked to his California work period. His surprise bill: over $15,000.

Fix:

6. ESPP Qualified Disposition Misses

The trap: Selling ESPP shares too early converts tax-favored gains into ordinary income.

Example: Tom sold after six months, losing around $1,200 in potential savings.

Fix:

7. Concentration Risk from “Never Selling”

The trap: Holding stock forever to avoid taxes often destroys more wealth than it saves.

Example: Lisa held $400,000 in company stock. A 40% decline wiped out $160,000 — far more than the $60,000 tax she was trying to avoid.

Proof: Multiple studies show most individual stocks underperform broad indexes over time — another reason to diversify concentrated company stock.

Fix:

Step 1: Calculate your true tax rate

Include federal, state, and payroll taxes. Don’t rely on company withholding.

Step 2: Build a systematic selling plan

Step 3: Time option exercises wisely

Step 4: Use tax-efficient strategies

Step 5: Coordinate with a professional

If annual equity exceeds $50,000, or if you’re facing AMT/multistate issues, professional tax planning can often save more than it costs.

Tech professional in California (RSUs + ISOs):

Emily earns a $250,000 salary plus $200,000 RSUs annually at a Bay Area startup. By selling 50% of each vest, she covers her tax bills and reduces stock risk. She exercises ISOs gradually each year to avoid AMT spikes, guided by financial professionals..

Dual-income family relocating (RSUs + ESPP):

Mark and Jenna earn $400,000 combined, with RSUs vesting while living in California. They’re moving to Texas. By timing their exercises and documenting work history, they limit California’s tax reach and optimize ESPP holdings for long-term gains.

*All examples are for illustrative purposes only and do not depict actual client scenarios.*

When do I owe taxes on RSUs — at vesting or at sale?

At vesting. The full market value is taxed as ordinary income, even if you hold the shares.

Can I avoid AMT on ISO exercises?

Not entirely. But you can minimize it by spreading exercises across years, using AMT calculators, and exercising in lower-income years.

What’s the best RSU selling strategy?

Many sell 40%-60% immediately to cover taxes and diversify, then hold the rest for long-term gains. The right mix depends on your goals, cash flow, risk appetite, and tax bracket.

How do state taxes affect equity compensation?

Top state income tax rates reach 13.3% in California; several states levy no individual income tax (e.g., AK, FL, NV, SD, TN, TX, WA, WY, NH).

Do I need a professional if my equity comp is under $100,000 per year?

Probably not — simple RSU cases can often be handled with calculators. Professional guidance can help prevent costly mistakes when dealing with more than $100,000 or with ISOs, ESPPs, or relocations.

This material has been prepared for informational and educational purposes only. It is not intended to provide, and should not be relied on for, investment, tax, legal, or accounting advice. Please consult your own financial advisor or tax professional before making any decisions. Domain Money does not provide investment advisory services or sell financial products. Domain Money is a Registered Investment Advisor with the SEC.

This story was produced by Domain Money and reviewed and distributed by Stacker.

Reader Comments(0)