The people's voice of reason

The people's voice of reason

Investing can often feel like navigating a maze of endless options and ever-shifting market conditions. This is where the Modern Portfolio Theory (MPT) comes in, offering a roadmap for making smarter investment decisions. Developed by Harry Markowitz in the 1950s, MPT has become a cornerstone of investment management, providing a framework to construct portfolios that maximize returns for a given level of risk.

Definition: MPT is a mathematical framework of investment decision-making that quantifies the relationship between risk and return in financial markets. It provides investors with a systematic method to construct portfolios that maximize expected returns for any given level of risk tolerance.

At its core, MPT is based on the idea that risk and return are inherently linked and that by carefully selecting a diverse mix of assets, investors can optimize their portfolios to achieve the best possible returns while minimizing risk. This is in contrast to traditional investing approaches, which often focus on picking individual stocks or timing the market.

In this guide, Range breaks down this Nobel Prize-winning theory into practical insights you can use to build a more efficient investment portfolio.

At the heart of MPT are a few key concepts that every investor should understand:

One of the central tenets of MPT is that there is a direct relationship between risk and expected return. In general, investments with higher potential returns also come with higher risks. MPT distinguishes between two main types of risk:

Diversification is the practice of spreading your investments across a variety of asset classes, sectors, and geographic regions to minimize risk. By including assets with low or negative correlations (for example, assets that tend to move in opposite directions), investors can potentially offset losses in one area with gains in another.

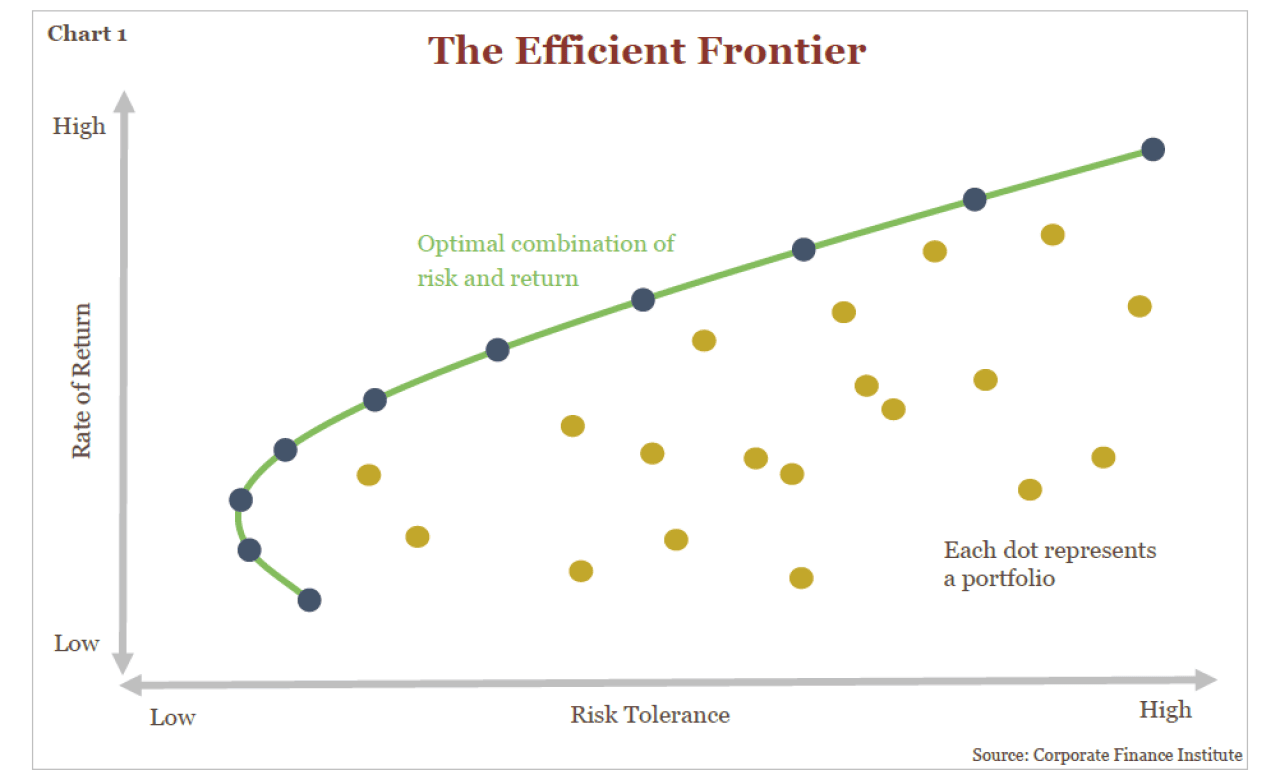

The efficient frontier represents the set of optimal portfolios that offer the highest expected return for a given level of risk or the lowest risk for a given level of expected return.

Portfolios that lie on the efficient frontier are considered the most efficient, as they provide the best possible tradeoff between risk and return. MPT aims to identify the best possible portfolio on the efficient frontier that aligns with your specific risk tolerance and financial goals.

Asset allocation strategies

Asset allocation is the process of dividing an investment portfolio among different asset categories, such as stocks, bonds, and cash (this includes savings accounts and other liquid accounts), based on their correlation to each other.

For example, stocks and bonds often have low correlations, meaning they tend to move differently in various market conditions. By combining assets with low correlations, investors can potentially smooth out their portfolios' performance over time.

Diversification techniques

Within each asset class, investors can further diversify their holdings by:

MPT introduces the concept of risk-adjusted returns, which consider an investment's return and the risk taken to achieve it. One common measure is the Sharpe Ratio, which compares an investment's excess return (return above a risk-free rate) to its volatility. A higher Sharpe Ratio indicates a better risk-adjusted return.

Other performance metrics, such as Alpha and Beta, also help investors compare the risk-adjusted performance of different portfolios or investments.

Portfolio optimization is selecting the best possible allocation of assets to maximize the expected return for a given level of risk. This involves looking at the expected returns, volatility, and correlations of various assets and using mathematical models to identify the optimal portfolio on the efficient frontier.

Implementing modern portfolio theory can:

While MPT has revolutionized the investment landscape, it's important to acknowledge its limitations:

Researchers have developed various extensions and modifications to MPT in response to these limitations, such as the Capital Asset Pricing Model (CAPM) or the Arbitrage Pricing Theory (APT). These models attempt to address some of MPT's shortcomings by incorporating additional risk factors and market dynamics.

Implementing MBT in your own investment portfolio involves:

Sophisticated software and algorithms can now analyze vast market data in real time, helping investors make better, data-driven investment decisions.

Artificial intelligence and machine learning techniques are specifically used to enhance portfolio optimization, risk assessment, and market forecasting. These tools can identify patterns and insights that traditional methods may miss.

What’s more, technology platforms offer portfolio optimization and monitoring features designed to ensure investors maintain properly balanced, diversified, and tax-efficient portfolios.

What is the main goal of MPT?

The main goal of MPT is to maximize the expected return for a given level of risk by optimally allocating assets within an investment portfolio.

How does MPT reduce risk?

MPT reduces risk through diversification, spreading investments across various asset classes, sectors, and geographic regions to minimize the impact of any one investment or market event.

Who invented MPT?

MPT was developed by economist Harry Markowitz in the 1950s. Markowitz's work laid the foundation for modern investing, earning him a Nobel Prize in Economic Sciences.

How do you apply MPT?

To apply MPT, assess your risk tolerance and investment goals. Then, use mathematical models to determine the ideal asset allocation for your portfolio. Regularly monitor and rebalance your portfolio to maintain your desired risk-return profile.

This story was produced by Range and reviewed and distributed by Stacker.

Reader Comments(0)