The people's voice of reason

The people's voice of reason

In April 2025, Freedom Debt Relief reviewed data from tens of thousands of people actively looking for help with their debt. The numbers might be surprising.

This report examines debt collection in the U.S. It shows which states have the most debt and what this means for American families' finances.

Key takeaways:

A collection account is a debt your original creditor has sold to a debt collection agency. Creditors, like banks or credit card companies, usually send your account to collections if payments are late for 120 or 180 days.

It’s sometimes a good idea to pay off a collection account in full. If that’s not possible, you have other options. For example, you could negotiate with debt collectors yourself, or join hands with a debt settlement company that bargains with a debt collector for you.

In April 2025, about one in four people looking for debt relief had at least one account in collections. The average collection balance is $3,027, spread across nearly one to two collection accounts.

Signs point to financial issues being tied to credit card debt. For those in need of debt relief, there is an average of 14 open tradelines, including more than five credit cards and $8,500 in credit card debt.

Furthermore, if someone’s financial picture matches that of the average American with debt in collections, the average credit utilization rate is 89%. Having credit cards that are maxed out (or close to it) is a red flag and means the user is leaning too heavily on credit, probably since before their accounts went to collections.

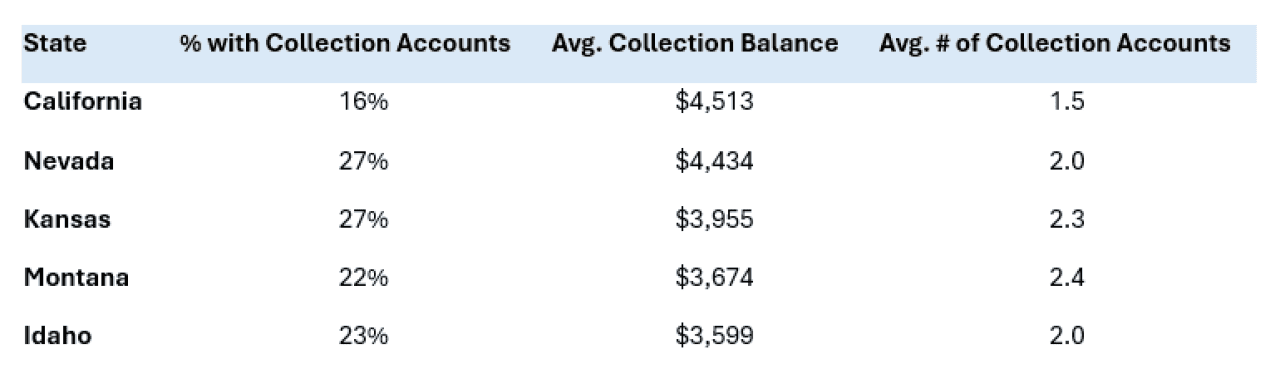

Check out how each state stacks up to the average collections debt figure. The table below highlights the five states with the highest average balances among people seeking debt relief in April 2025.

Biggest debts

The Golden State takes the cake for the most expensive debts. California tops the list, with an average collection balance of $4,513. However, only 16% of people in the state have an account in collections.

More debt relief seekers in collections

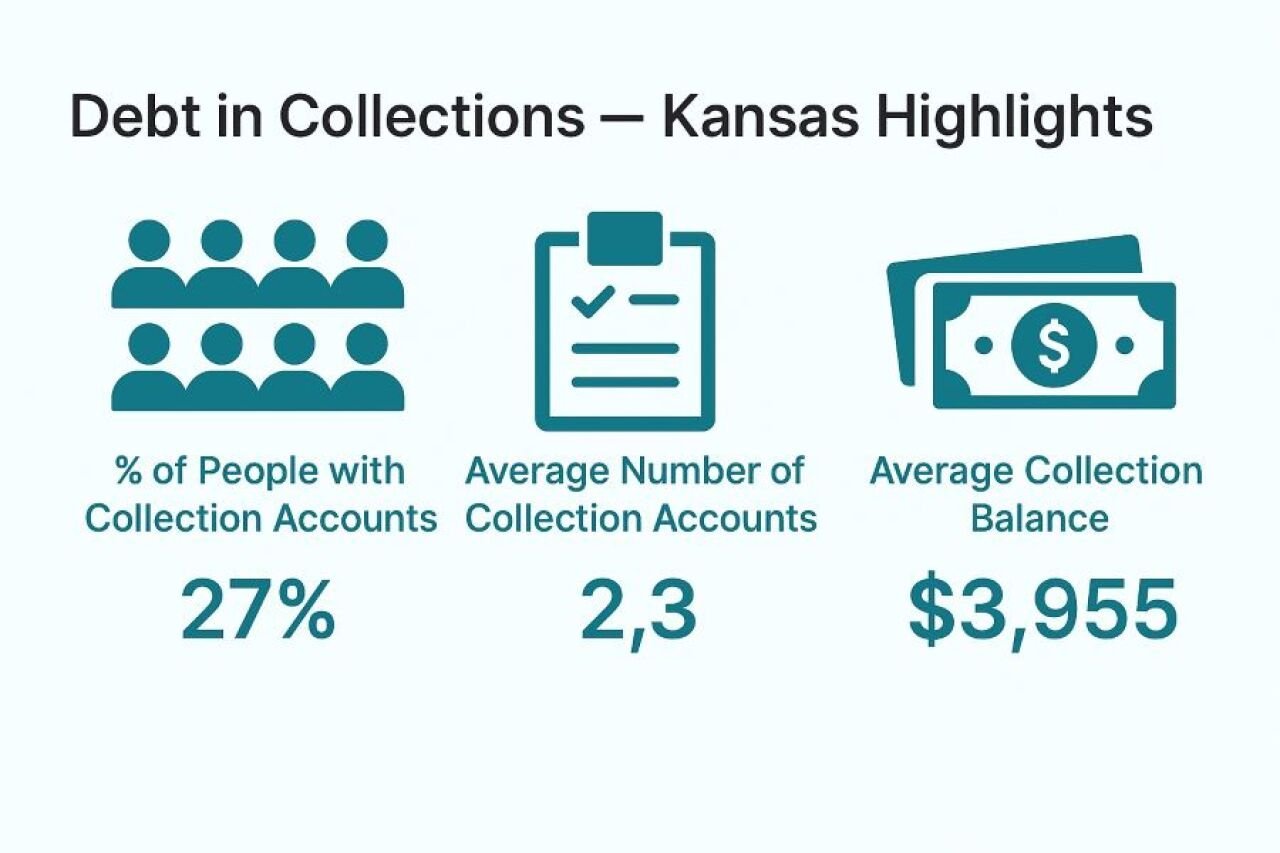

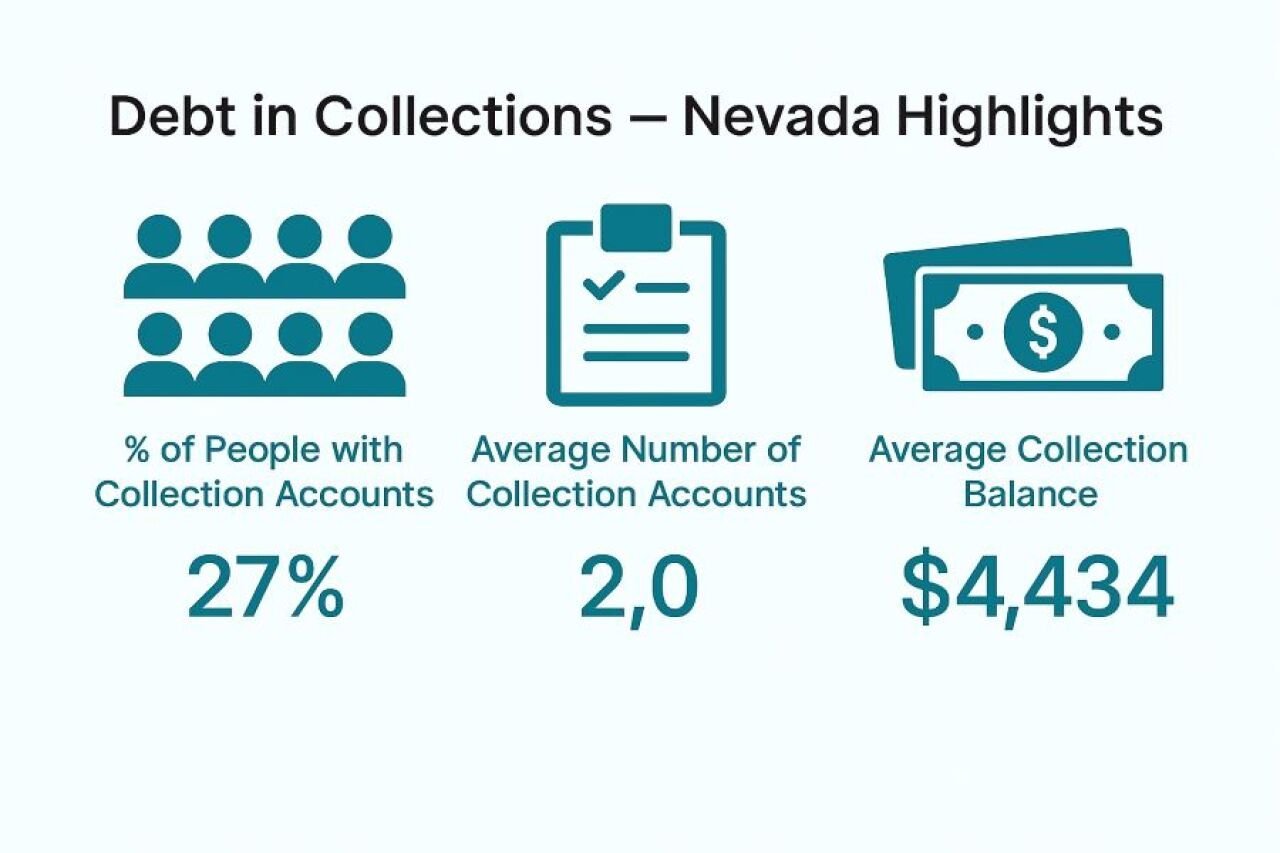

In contrast, Nevada and Kansas have significantly higher proportions of people with debt in collections—27% in both states—and sizable average balances over $3,900.

Highest number of collection accounts

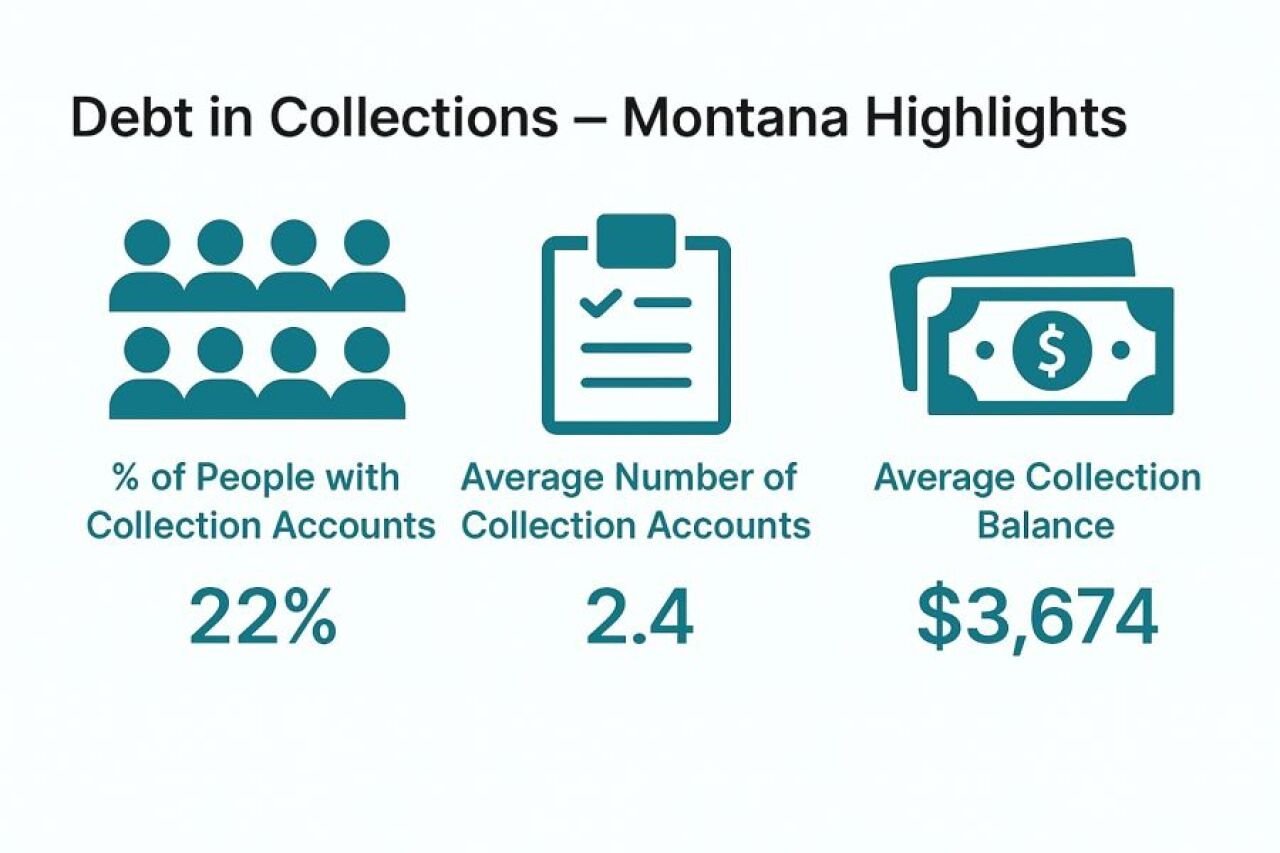

More than one debt in default: Montana and Kansas showed the highest average number of collection accounts per person, with 2.4 and 2.3, respectively.

These patterns point to different types of risk across states. In some places, fewer people have accounts in collections, but the ones who do owe more. In other cases, collections are more widespread, with people juggling multiple delinquent accounts.

Credit card debt and collection accounts are closely linked, like two peas in a pod. Most of the debt relief seekers in this analysis have high credit card balances, often maxed out.

This is because credit cards are typically the first resource when people don’t have enough in the bank to pay bills. Over time, carried balances build interest. Sometimes, people fall behind, and their credit card debt can be sold to collection agencies.

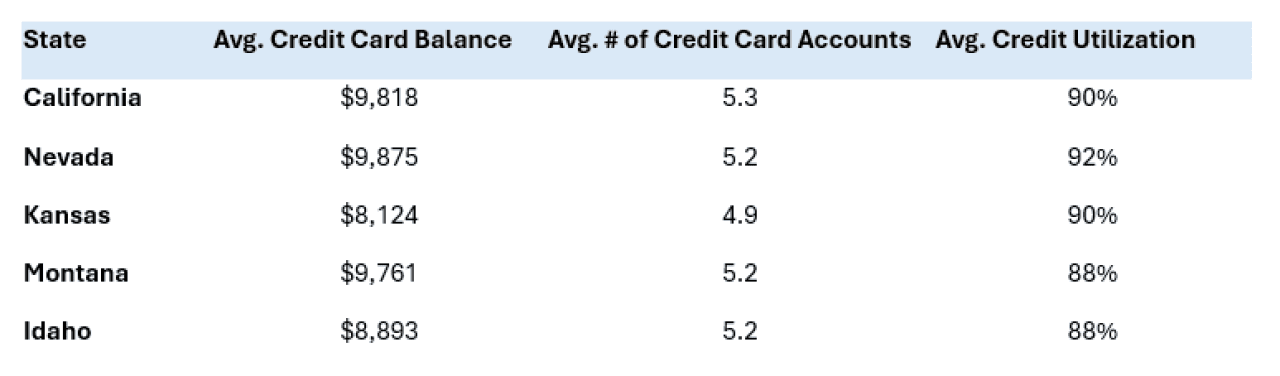

Of those surveyed, the table below highlights the average credit card balance by state.

Credit card balances are high among those looking for debt relief. Across the board, they range from just over $8,000 to nearly $10,000.

Owning multiple cards is the norm. The average person in each state has around five open credit cards, and utilization is extremely high—between 88% and 92%.

These numbers show that before someone defaults on debt, they probably rely a lot on credit for daily expenses or emergencies. For many, collections may have been the result of an already maxed-out financial situation.

Debt in collections - California highlights - April 2025

Debt in collections - Kansas highlights - April 2025

Debt in collections - Montana highlights - April 2025

Debt in collections - Idaho highlights - April 2025

Debt in collections - Nevada highlights - April 2025

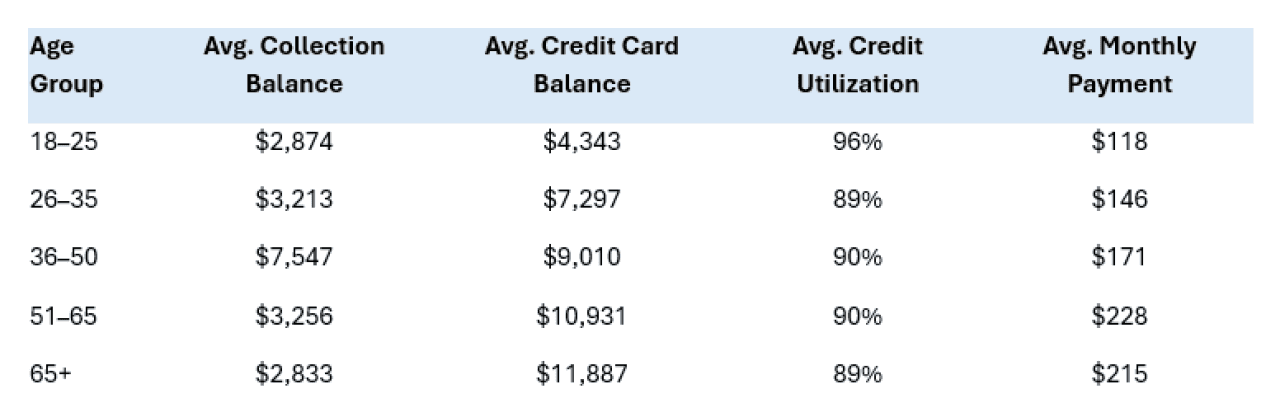

Let’s dig deeper into collection accounts to sort debts by age. Despite some overlap, older and younger Americans have very different situations.

Balance sizes peak in middle age. People ages 36–50 have the highest collection balances, owing more than double the average of most other groups. At this age, people are likely to reach the point where they spend big bucks on housing and kids.

Meanwhile, older adults (51–65 and 65+) have the highest credit card balances, but lower collection balances. That could reflect more available credit and a better payment history.

Younger people (18–25) show very high utilization (96%) even though their balances are relatively low—suggesting they’re maxing out low credit limits. It’s easier to max out cards when you’re capped at $1,000, a relatively low credit line.

Monthly payment amounts rise with age and peak in the 51–65 group—consistent with higher income or credit limits. At this age, some might also have a strong resolve to start paying down those balances..

When dealing with debt in collections:

This story was produced by Freedom Debt Relief and reviewed and distributed by Stacker.

Reader Comments(0)