The people's voice of reason

The people's voice of reason

It’s impossible to ignore the gnawing presence of inflation, as it infiltrates almost every aspect of daily life, from the price we pay for groceries to the cost of everything from travel and car maintenance to property and healthcare.

While the immediate impact grabs the most headlines, it’s the long-term effects that deserve even more attention, especially from the perspective of retirement savings.

Putting cash in an account that earns no interest is a recipe for losing money, as each passing day sees inflation eat away at the spending power it represents. The longer you wait to make your money work for you and protect it from the eroding power of inflation, the greater the scale of the damage done.

To measure the long-term impact of regional inflation on retirement savings, financial services firm Abacus Global Management analyzed data from the U.S. Bureau of Labor Statistics and modeled the growth of a hypothetical investment portfolio over 30 years. The analysis reveals how geography can significantly alter the real-world value of a retirement nest egg.

The Consumer Price Index (CPI) is the most useful way to measure inflation, and while typically it’s discussed on a country-wide basis, there are some stark differences between how this plays out regionally, which need to be addressed before we go any further.

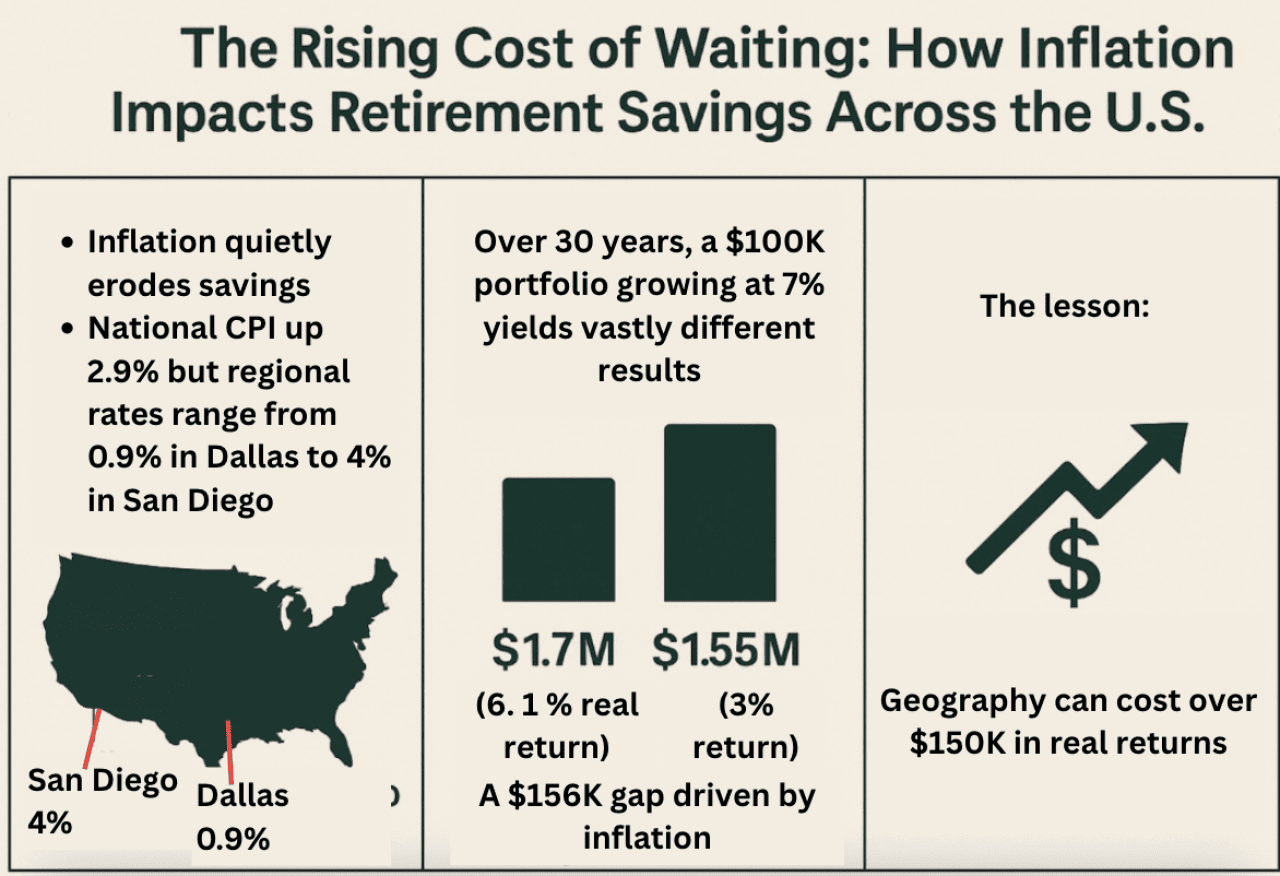

In August 2025, the CPI rose 2.9% year-over-year across all categories of items covered, which include, but are not limited to, food, energy, new vehicles, and clothing.

Between the regions, there’s much more variation. For the same month, the West South Central region sits at the lower end with a 2% CPI rise, while the rate for New England is a whopping 3.7%.

There’s also intriguing data from specific metropolitan areas. The CPI in Dallas-Fort Worth was up by just 0.9% in August, for instance. Meanwhile, the San Diego-Carlsbad area saw a 4% annual increase in prices across the most common consumer expenses.

In other words, the cost of living is creeping up more quickly in some places than others. And in turn, this is a pivotal talking point when it comes to retirement savings.

Before we can talk about how retirement savings hold up to the onslaught of inflation, it’s necessary to establish exactly how much of a return this type of account can expect to achieve.

Because retirement savings are a long-term proposition, with returns achieved over decades, there’s much debate over a reasonable average to expect. Annual averages of 12% over a 40-year period have been posited by many, but this is very much a best-case-scenario calculation that’s not deemed realistic by its critics. More conservative expectations of between 5% and 7% are reasonable.

So far, so good. If your retirement savings grow by 5% a year, this means they are increasing at a rate above the 2.9% increase to the national CPI seen in August 2025.

Of course, the regional variations outlined earlier can’t be ignored in this context. Someone who lives in San Diego who’s saving for retirement will see their savings growth eroded almost entirely. At the same time, a resident of Dallas, Texas, can be confident of seeing a far more negligible impact.

To put this in perspective:

As mentioned earlier, San Diego’s inflation has seen a 4% rise year-over-year, while Dallas sits at a modest 0.9%. Let’s say that you have a $100,000 retirement portfolio that grows at a modest rate of 7%.

When planning for retirement, you have to consider the real rate of return, which is the annual return minus the rate of inflation. With a 7% growth rate, and given the inflation rates of the two cities mentioned, your return after 30 years would be:

That’s a difference of $156,543, which is higher than the initial amount of your retirement portfolio.

Coupled with the fact that higher inflation in certain regions leaves locals with less disposable income to put aside for retirement or a rainy day, the problem is compounded further.

The main takeaway is that retirement savings must be properly protected from the short-term and long-term influence of inflation, no matter where you live. The need to do so may be more pressing in places where living costs have a tendency to rise precipitously, but it’s a lesson everyone benefits from learning.

Having savings accounts with solid returns is a good starting point. However, avoiding exposure to market volatility as well as the erosive power of inflation requires diversification. Exploring a variety of asset classes and planning for retirement with calculations that take into account the need to live comfortably, not just pay basic bills, puts people in the best position.

This story was produced by Abacus Global Management and reviewed and distributed by Stacker.

Reader Comments(0)