The people's voice of reason

The people's voice of reason

Maximizing cash flow is always the goal for real estate investors. But many are leaving cash on the table by opting for standard depreciation instead of bonus depreciation for qualifying properties.

Bonus depreciation is a powerful tax savings strategy that, thanks to software and automation, is now accessible to any rental property owner and their accountant. With it, rental property owners can write off a large portion of their property costs in year one of service, massively front-loading tax savings and boosting their bottom line.

In this guide, TurboTenant will explain:

Bonus depreciation is an accelerated tax deduction that allows you to deduct 100% of the cost of specific components of your investment property in year one of service. Bonus depreciation is available for “qualified property” within your larger property as a whole. This could include appliances, a fence, light fixtures, and other similar components, but doesn’t include the structure or land itself.

The standard rental property depreciation method involves deducting the cost of the entire property over 27.5 years. However, a significant portion of that cost (typically around 20%-40%) can be depreciated in the first year of service, thanks to bonus depreciation.

If you purchase a $1 million property, that means you could deduct an additional $200,000-$400,000 in bonus depreciation expenses in the year you bought it. With standard depreciation, that number would only be around $36,000. Bonus depreciation creates a significant tax incentive for real estate investors to buy more properties, enabling them to deduct more upfront expenses against their business income.

Keep in mind that these assets are eligible for bonus depreciation in year one of service, not just for new purchases. If you improve your property by putting in new appliances, light fixtures, or fencing, those improvements would be eligible for bonus depreciation in the year you built them.

Bonus depreciation was first introduced in the Tax Cuts and Jobs Act of 2017. It started at 100%, but was set to phase out by 20% each year, reaching 0% by 2027. This phase-out timeline made tax planning for bonus depreciation more complicated and reduced the incentive to take advantage of it.

However, in 2025, the One Big Beautiful Bill Act (OBBBA) reinstated 100% bonus depreciation and made it permanent. At least for now, full bonus depreciation has returned and isn’t phasing out. This should encourage investors to purchase more rental properties and may even help increase the plateauing real estate prices we’ve seen due to higher interest rates.

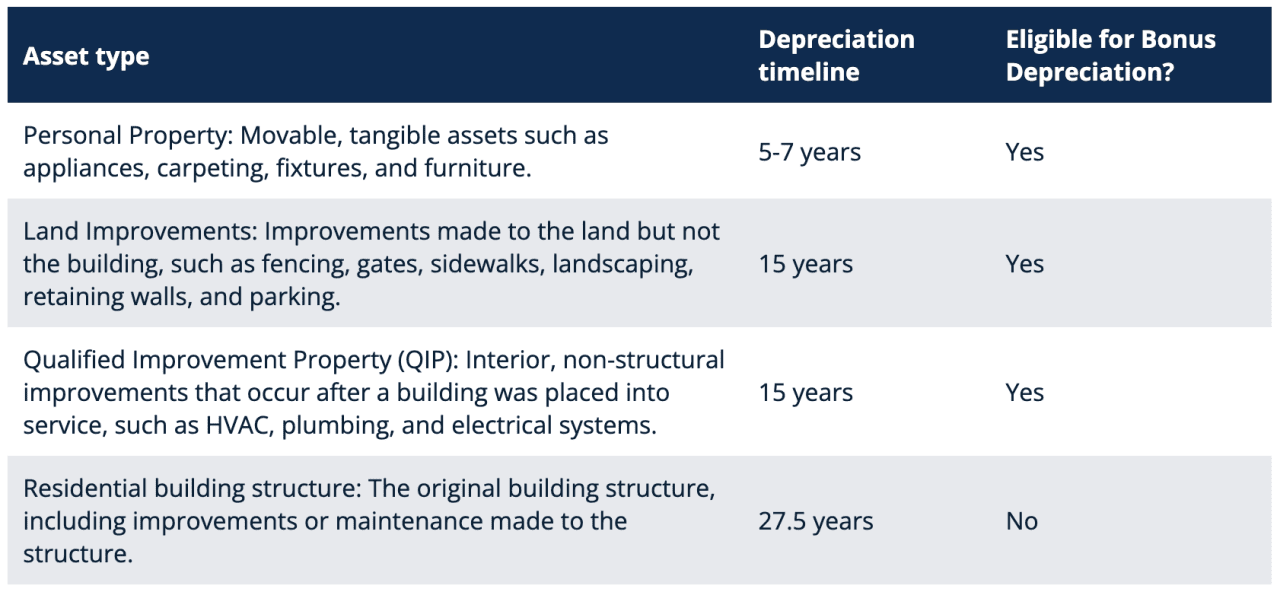

Not every part of your property will qualify for bonus depreciation. The extra deduction only applies to assets with a Modified Accelerated Cost Recovery System (MACRS) life of 20 years or less.

In simpler terms, parts of your property are eligible for shorter than 20-year depreciation periods, while others are only eligible for the standard 27.5-year depreciation. Only the parts that can be depreciated in less than 20 years are eligible for bonus depreciation.

Personal property, land improvements, and specific nonstructural improvements all qualify for depreciation periods of 20 years or less. The structure itself, however, is only eligible for 27.5-year depreciation, meaning it doesn’t qualify for bonus depreciation. Typically, around 20%-40% of a property’s value is eligible for bonus depreciation, while 60%-80% is not.

The table below shows which asset types are eligible for 100% bonus depreciation and which are not.

To break your property down into different categories and find out what’s eligible for bonus depreciation, you need to do a cost segregation study.

Officially recognized by the IRS, cost segregation studies traditionally required an engineer to come to your property and take copious notes and photographs. The engineer meticulously records what qualifies as different categories and what is eligible for accelerated depreciation timelines. Finally, they deliver a cost segregation study report that you can hand over to your accountant to enter into your tax return, which could also be a complex process.

The cost of traditional cost segregation studies ranges from $5,000 to $15,000 for typical residential properties, and may be significantly higher for larger properties. However, automation and software have made cost segregation studies more affordable and accessible to smaller real estate owners.

You can now use AI-driven cost segregation software, such as Segtax, to automate the majority of the process. These programs are IRS-compliant and significantly reduce the cost and time required for cost segregation, making it easier for smaller real estate investors to take advantage of bonus depreciation.

Let’s do a simple example to show the tax savings impact that bonus depreciation makes.

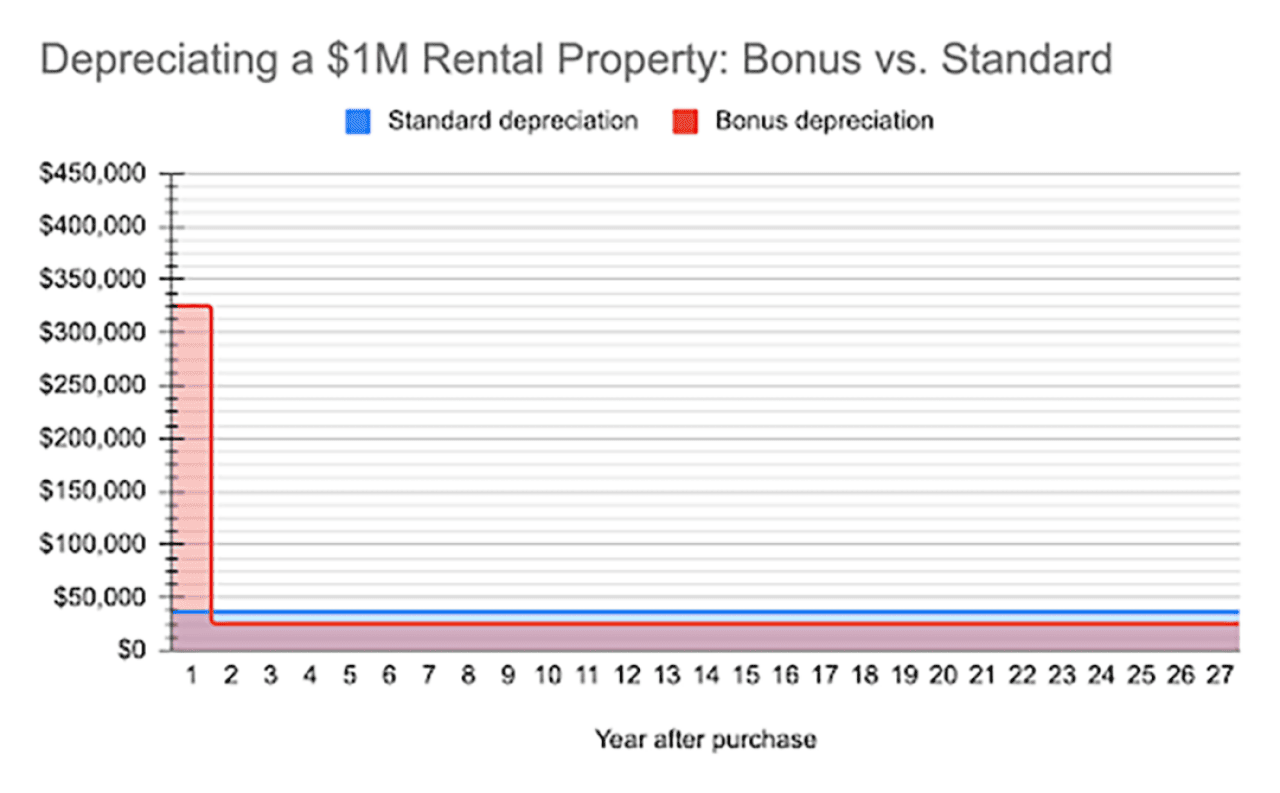

Say you purchased a $1 million rental property and completed a cost segregation study. The study found that 30% of the property’s value consisted of personal property and improvements that are eligible for bonus depreciation.

In the first year after the purchase, you can use bonus depreciation to deduct $300,000 from your taxes, resulting in significant tax savings. You also get to deduct the remaining $700,000 over the standard 27.5-year period, so your total depreciation deduction for year one ends up at $325,455. For the next 26.5 years, you can only deduct the remaining $700,000, which is $24,455 per year.

By comparison, if you used the standard depreciation, you would deduct $1 million over 27.5 years, which comes to $36,364 per year. Still some tax savings, but nowhere near as much as bonus depreciation in year one.

Below is a chart showing the staggering difference in year one and how the amounts change in the remaining years. Most investors would take the tax savings now rather than later, so they can reinvest them in more properties, which would also have components eligible for bonus depreciation.

Before the advent of automated cost segregation studies and easy-to-use rental property accounting tools, the benefits of accelerated depreciation were reserved for wealthier property owners only. Not only were cost segregation studies expensive, labor-intensive, and lengthy, but accounting for various depreciation timelines was much more complicated.

Now, with more tech-forward solutions, rental property owners of any size (and the accountants that serve them) can easily take advantage of the tremendous tax savings that bonus depreciation offers. Even for just one property, bonus depreciation makes a big difference, and these tools make it feasible for any property owner to access those savings.

The OBBBA is a boon for rental property owners who can take advantage of it. However, American politics is in constant flux, and tax laws can change every four years. Owners and accountants would be wise to strike while the iron’s hot and start taking advantage of bonus depreciation as soon as they can.

If you’re a rental property owner or accountant who serves them, here are some steps you can take now to take advantage of bonus depreciation opportunities.

This story was produced by TurboTenant and reviewed and distributed by Stacker.

Reader Comments(0)