The people's voice of reason

The people's voice of reason

Did you just look at your bank account and say, “Where am I going to find the money to pay for that?” The new refrigerator, the medical procedure that is going to cost an arm and a leg, the soccer camp, the auto repairs … the list goes on and on.

Before you pull out your credit card or go down to the local pawn shop, take a look at how an unsecured personal loan could help you meet your financial goals.

Key Takeaways:

Not sure how? Achieve breaks it down.

An unsecured loan is a loan you get based on your creditworthiness. Unlike secured loans, which provide money to borrowers with assets (houses and cars, for example), unsecured loans do not require any assets or collateral.

Unsecured personal loans are considered installment loans. That means you borrow a set amount at a fixed interest rate that won’t change for the life of the loan. That’s really important in times when interest rates go up. You’ll pay off the loan in equal monthly payments over a time period that is determined when you get the loan.

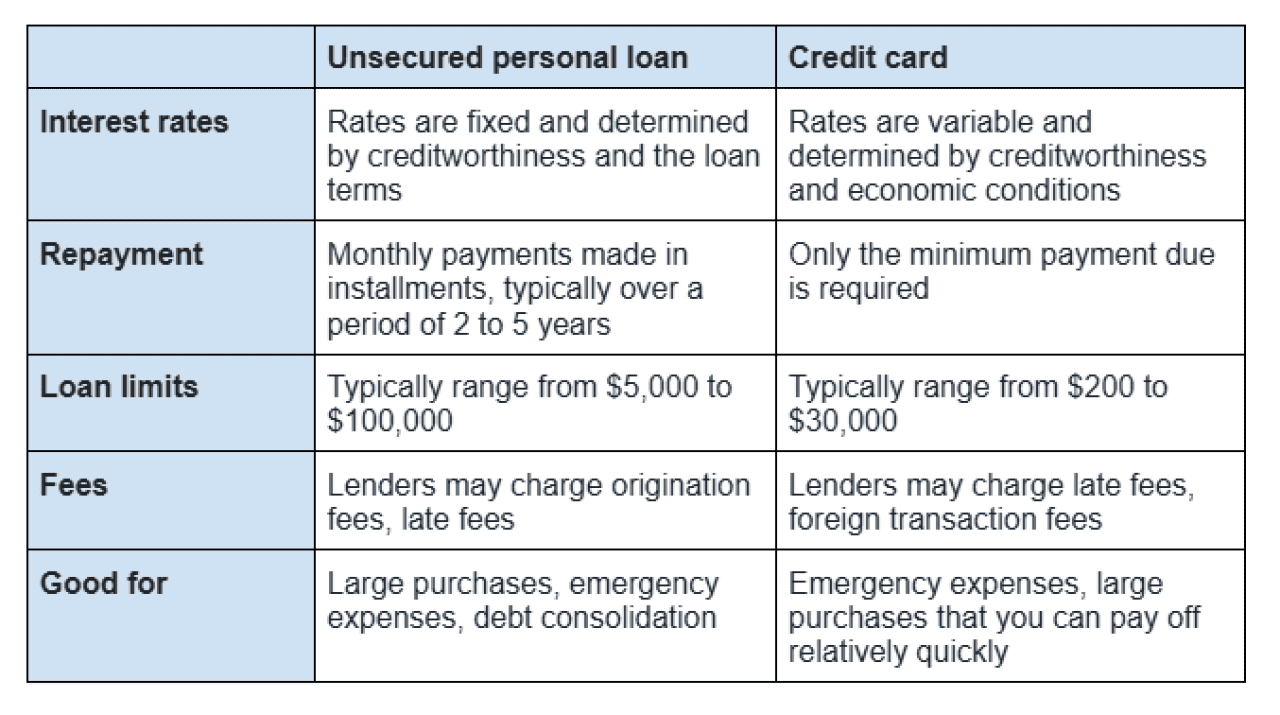

Unsecured personal loans and credit cards both allow you to borrow money, though they don't work the same way.

There are several important differences between an unsecured personal loan and credit card charges.

How much can you borrow with a personal loan vs. a credit card?

With a personal loan, you get a fixed loan amount that's based on several factors, including your creditworthiness. Credit cards, on the other hand, come with a set limit that represents the maximum amount you can charge.

Compared to personal loans, credit card limits are typically lower. For instance, you might be able to get a $50,000 personal loan, but your credit card limit may be capped at $5,000 or $10,000.

Limits on credit cards start as low as $200, and can be as high as tens of thousands of dollars. The loan amount for unsecured personal loans could be anywhere from $1,000 to $100,000, but most tend to range from $5,000 to $50,000.

Credit cards are also known as revolving credit because as you pay off your charges, you can make more purchases. After each billing cycle, you could choose to pay off all of your charges or carry the balance over to the next month.

If you have a balance on your credit card, you will need to pay a minimum amount due each month. That could be much less than the required monthly payment amount for an unsecured personal loan. In this way, borrowing and spending can go on indefinitely.

An unsecured personal loan doesn’t work like that. You’ll borrow money one time and pay it back in installments with interest. Your loan balance only goes down, not up, until it's paid off completely.

The repayment period for a personal loan is typically between two and five years, but some lenders offer longer options. The repayment period for a credit card, meanwhile, could go on … well, forever.

Both credit cards and personal loans can charge interest, though rates can vary widely.

Credit card interest rates are variable, which means they can increase or decrease as the overall interest rate environment changes. It’s normal to have a credit card interest rate that’s 20% to 36%, though it's possible to find cards that offer a low 0% introductory rate for a set period. Once the introductory rate expires, the regular rate applies.

Unsecured personal loans also charge interest, but the interest rate won’t change. Personal loan rates could be much lower than the rate on your credit card if you have good to excellent credit.

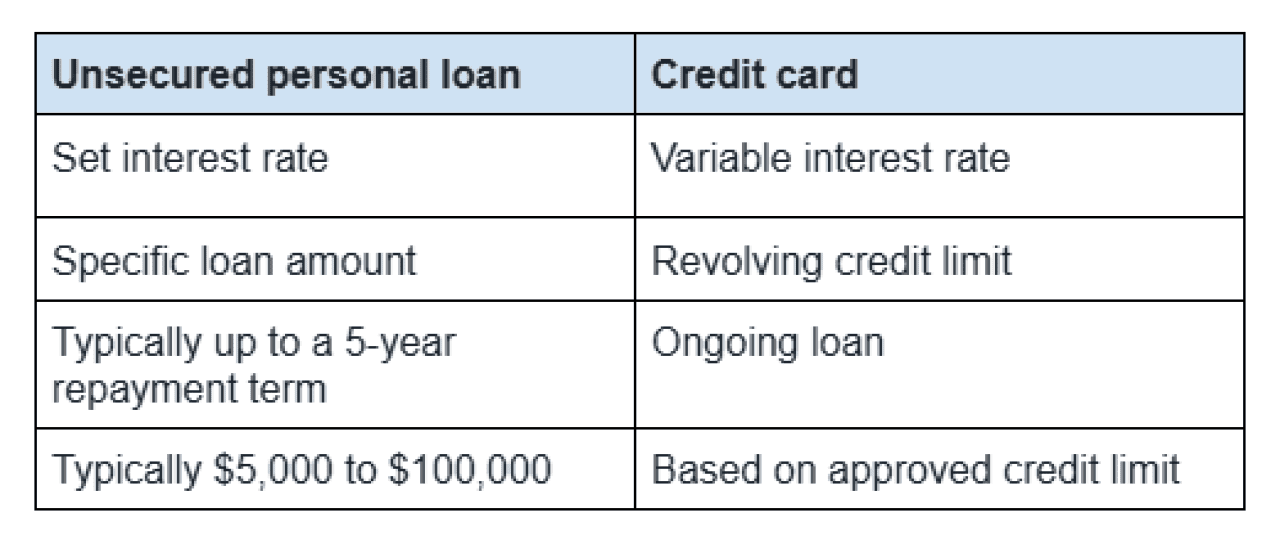

Here’s a quick way to see the differences between unsecured loans and credit cards:

Personal loans are flexible since they can be used to meet a wide range of financial needs. Here are some common uses for an unsecured loan.

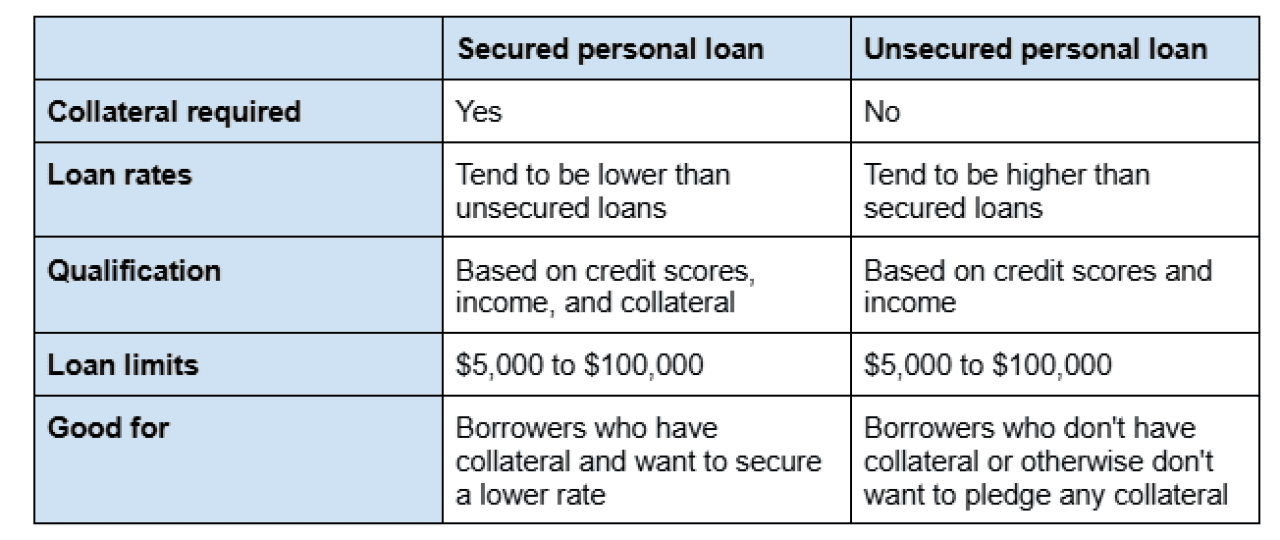

The interest rate for your unsecured personal loan will depend on your credit rating. As a general rule, unsecured personal loan rates tend to be higher than rates for secured personal loans.

That’s because with a secured loan, the lender gets your collateral if you default. With an unsecured loan, they would be stuck with the loss. So the rates are typically higher for unsecured loans to make up for that.

Unsecured loans may also be harder to qualify for, since there's no collateral on the line. But if you have a history of repaying your debts and your credit score is fair or better, you might qualify for an unsecured loan.

How do you get a low rate on a personal loan? It starts with some homework.

Compare personal loan options from multiple lenders and look at:

Look for lenders that offer rate quotes without any impact on your credit. You can use these quotes to estimate what you'll pay in interest and what your monthly payment will work out to.

Here are a few tips to pay less for a personal loan:

Also, ask about personal loan interest rate discounts that could lower your cost, including:

Qualifying for these discounts on a personal loan through Achieve could result in savings.

The process to apply for a personal loan is relatively straightforward. You'll first need to find a lender, then complete the necessary paperwork. Here's an overview of how it works.

Get prequalified. Prequalification means a lender has done an initial review of your financial situation and offered a tentative loan approval. Prequalification is not a guaranteed loan offer, but it can give you an idea of what you might be able to borrow.

Personal loans have advantages and disadvantages to consider before you borrow. Here's a quick look at how the pros and cons compare.

Personal loan pros

Personal loan cons

We've already talked briefly about secured loans and how they differ from unsecured loans concerning collateral and interest rates. Here's a recap of what you should know about the two.

A co-signer is someone who applies for the loan with you and agrees to be held legally responsible for it. Your co-signer may not make any payments toward the loan if you agree to do so. But if you default, the lender could come after you and your co-signer to collect what's owed.

What are the benefits of using a co-signer for a personal loan?

Are there downsides to having someone co-sign a loan? The biggest risk is damage to their credit and your relationship if you default.

Your co-signer may not appreciate their inclusion in a debt lawsuit if the lender sues you both over an unpaid loan. Their credit (and yours) could take a hit, which could make it harder for them to get loans elsewhere.

For those reasons, it's important to be sure you can afford the payments before you get a personal loan with a co-signer.

Lenders decide who to offer unsecured personal loans to based on several factors. Typically, personal loan requirements extend to:

Why these factors? Lenders want to make sure you have enough money to make your monthly loan payments and that you're likely to pay on time. They use your credit scores as a guide to gauge your creditworthiness or level of responsibility when it comes to debt.

The minimum credit score for a personal loan is typically in the 620-660 range, though it may be higher with some lenders. The better your credit score, the easier it may be to qualify for an unsecured personal loan and get a lower rate.

When you need a personal loan, it's okay to take your time. The right personal loan for you offers the best terms and the amount of money you need to borrow.

Here are a few tips you can use to choose the best unsecured personal loan for your situation.

Before you apply for a personal loan, check your credit. That can give you an idea of whether you might need a co-signer to qualify and what rates you may be eligible for.

Personal loans are just one way to get cash when you need it. You could also explore other ways to borrow, which might include:

Each one has pros and cons. Credit cards, for example, are convenient, but they can carry high interest rates. A home equity loan or HELOC can offer lower rates, but they require you to use your home as collateral to borrow. That means if you don't repay the loan, you could lose your home.

Retirement plan loans can give you ready access to cash but they could shortchange your retirement savings in the long run. And loans from friends and family may be interest-free, but they could turn a relationship sour if you don't repay what you borrow.

The best way to decide whether to choose a personal loan or another loan option is to consider what you need the money for and how you'd prefer to repay it. At the end of the day, unsecured personal loans can meet your financial needs with fewer hassles than other loan options.

What is the difference between a secured and unsecured loan?

A secured loan requires collateral. Collateral is something valuable that you pledge as a guarantee that you’ll repay the loan. If you don’t repay the loan, you could lose the collateral. A common example is a house, which is the collateral for a mortgage. Collateral is a financial safety net for the lender.

With an unsecured loan, you qualify based on your credit standing and the financial information you provide. If you fail to repay the loan, the lender can’t take anything you own to cover its losses. Of course, they could (and probably will) pursue you in other ways for repayment of the loan.

Why does an unsecured loan have a higher interest rate than a secured loan?

Because they aren't attached to collateral, unsecured loans are a little riskier for the lender than secured loans. If something happens and you don’t repay the loan, the lender could lose money. In general, we pay more for financial products that lenders consider riskier. So if you were to shop on the same day for an unsecured personal loan and a car loan, the average interest rate for car loans would probably be lower than the average rate for personal loans.

How can I get a personal loan with a co-signer?

When you apply, tell the lender you have a co-applicant. This is usually a box to check when you apply online. It only takes a few minutes to fill out an online loan application. The lender will verify both people’s identities and income and will check both people’s credit.

This story was produced by Achieve and reviewed and distributed by Stacker.

Reader Comments(0)