The people's voice of reason

The people's voice of reason

The automotive past offered predictability. A typical fender bender meant a repair, a short rental, and a completed claim with the car insurance provider. Today, that same minor collision is increasingly likely to result in a "total loss" designation from the insurer. Even seemingly fixable damage leads to vehicles being written off at an alarming rate. This change is not due only to visible damage; it is the result of the "Total Loss Tsunami," driven by persistent global supply chain disruptions and soaring parts costs. This situation represents a significant financial hit for vehicle owners and a fundamental shift for the entire auto insurance industry. The rising frequency of total loss claims is a key driver behind increasing auto insurance premiums, a trend analyzed closely by resources such as Cheap Insurance.

The decision for a car insurance company to declare a vehicle a total loss boils down to a cold, hard calculation: Is the cost of repairing the vehicle more than a certain percentage of its Actual Cash Value (ACV)? This total loss threshold is set by state law or by the insurer, but typically hovers around 70% to 80% of the ACV. If repair costs hit that mark, the vehicle is totaled.

The application of this rule varies drastically by location, creating different risk profiles for vehicle insurance providers nationwide. For example, Oklahoma has one of the nation's lowest thresholds at 60%, meaning a vehicle with damage exceeding 60% of its value must be totaled. Conversely, states like Texas have a 100% threshold, though insurers there often use their own, lower economic threshold. This complexity means that the same repair cost on the same model of vehicle can lead to a total loss in one state but not another.

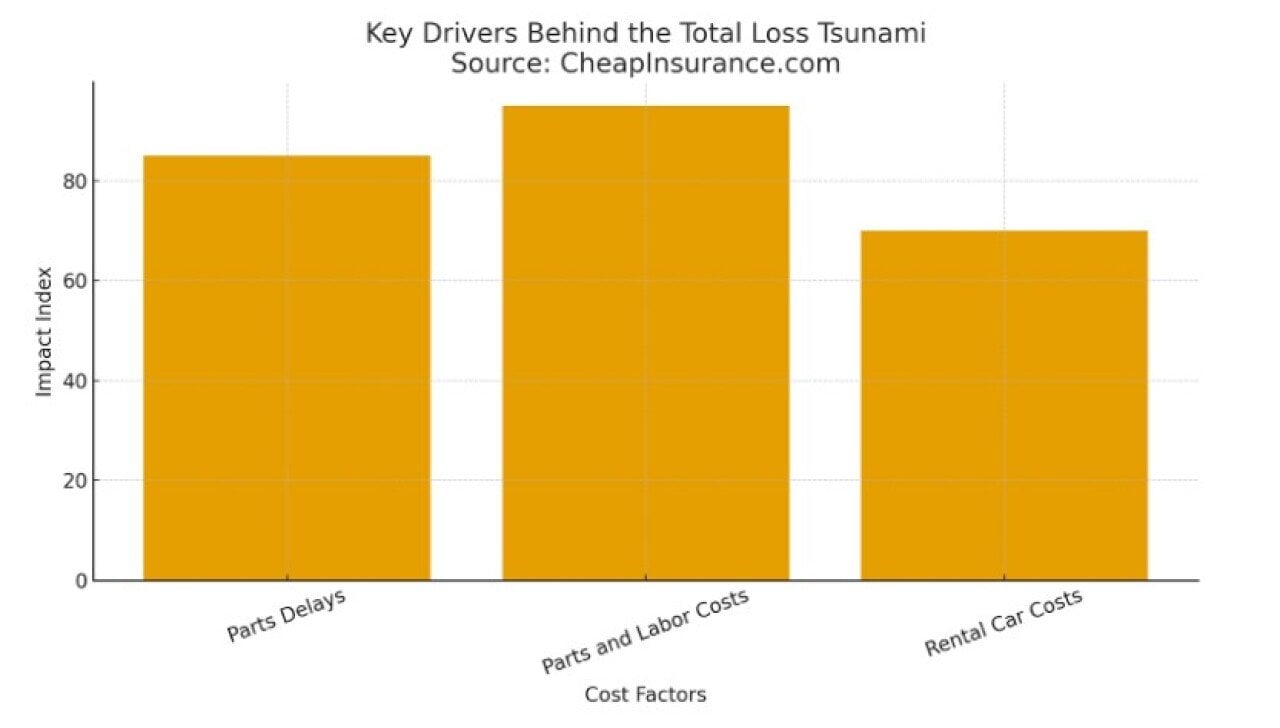

Before the pandemic, this calculation was relatively stable, allowing auto insurance providers to predict claim outcomes. Now, virtually every variable has been altered, making that total loss threshold far easier to breach for the insurer.

A vehicle needing a new bumper, a headlight assembly, and specific ADAS sensors faces severe challenges.

A repair job that once took two weeks can now stretch to two months or more simply waiting for parts, a delay that escalates the claim cost for the car insurance provider.

Scarcity is driving up claim severity, a major factor in rising auto insurance premiums.

These escalating costs push the repair estimate ever closer to that total loss threshold. A $7,000 repair on a car valued at $10,000 is becoming common, quickly crossing the legal total loss limit and forcing the hand of the car insurance company.

While a damaged vehicle sits in the repair shop's yard awaiting a single elusive part, the insured may be driving a rental car. The vehicle insurance company is generally responsible for this expense.

Most policies have limits on rental car coverage, such as a daily rate for a maximum number of days. If the repair is delayed to 60 or 90 days due to parts shortages, those extended rental costs quickly accumulate, sometimes adding thousands of dollars to the claim. When these extended rental costs are factored into the total repair equation, it further incentivizes the "total loss" decision. It becomes financially prudent for the car insurance provider to write off the vehicle rather than continue paying for a rental indefinitely.

The "total loss" equation is driven by the Actual Cash Value (ACV) of the vehicle, which is its worth before the accident, factoring in depreciation and mileage. Car insurance providers use this figure as the financial ceiling for any claim payout.

While recent used car values have been high, the rapid rise in repair costs often outpaces this appreciation. Many older vehicles simply have not retained enough ACV to offset skyrocketing repair estimates.

This valuation is further complicated by state law. For instance, California uses the Total Loss Formula (TLF), which declares a vehicle totaled if the cost of repairs plus the salvage value exceeds the ACV. This formula, used by car insurance companies, means that a vehicle can be totaled even if the repair cost alone is less than the ACV. Ultimately, the cost shock minimizes the insurer's total loss payout.

The Rise of the Total Loss trend has tangible, painful consequences for every party involved.

While owners cannot fix global supply chains, effective management of the car insurance policy and claim process can mitigate financial risk. Owners should take these proactive steps:

The era of predictable repairs is over. Understanding these financial forces and preparing the vehicle insurance file is the first step in protecting financial interests in this new automotive reality.

This story was produced by CheapInsurance.com and reviewed and distributed by Stacker.

Reader Comments(0)