The people's voice of reason

The people's voice of reason

The digital landscape in 2025 has ushered in a powerful new era for fraud, one in which bad actors can use artificial intelligence, deep-learning tools, and sophisticated social engineering tactics to scale scams across state lines. While many still picture scams as phone calls meant to trick those who don’t know any better, the reality today is that anybody can fall for a scam generated by AI. Understanding where these scams are concentrated can help consumers, policymakers, and enforcement agencies alike focus their efforts more strategically.

Lifeguard pulled together data from the FBI’s 2024 Internet Crimes Report to drill down state-by-state on where losses and scam complaints are the highest. Using this data, along with context on why certain states appear more vulnerable, can help all residents take action to reduce the risk of falling victim to AI-generated fraud.

The 2024 Internet Crime Report, issued by the Internet Crime Complaint Center division of the Federal Bureau of Investigation, reveals a record total of more than 859,000 scam complaints nationwide. In particular, phishing/spoofing, extortion, and personal data breaches topped the list with over 193,000, 86,000, and 64,000 complaints, respectively. The remaining complaints are as follows:

However, investment fraud led the way in terms of dollar loss, with more than $6.5 billion in reported losses. This type of scam typically involves cryptocurrency or other emerging assets related to it. This means that scams are evolving fast, often leveraging AI scripts, deepfake voices, and large-scale impersonations in an effort to trick you.

While phishing and spoofing, a deceptive tactic where someone impersonates a trusted source, may still dominate scam complaints in terms of numbers, the financial impacts from higher-severity frauds can be more devastating. Fake investment platforms, AI-generated “help desks,” and impersonations of relatives’ voices are all concerns that should now be on your radar.

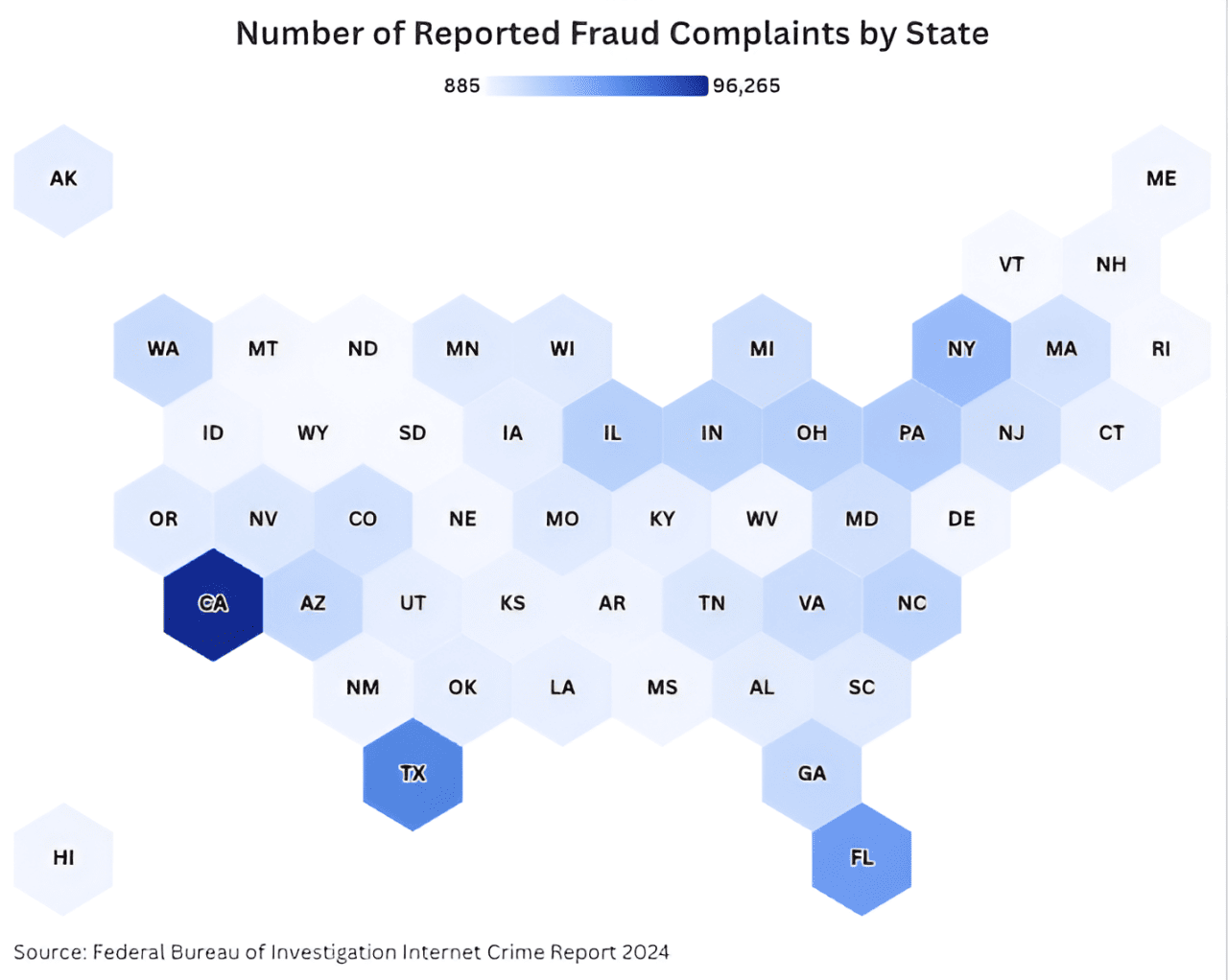

Drilling deeper into a state-by-state analysis of the data from the 2024 report, it’s clear that the number of reported fraud complaints is not evenly distributed across the country. This heatmap highlights where users file the most complaints, essentially signaling potential scam “hot spots”:

States with large populations and high digital connectivity tend to lead, with California, Texas, and Florida at the front. However, the “why” of the matter is more complex. There are a number of reasons these states see more scam activity beyond population and connectivity, with the most prominent being:

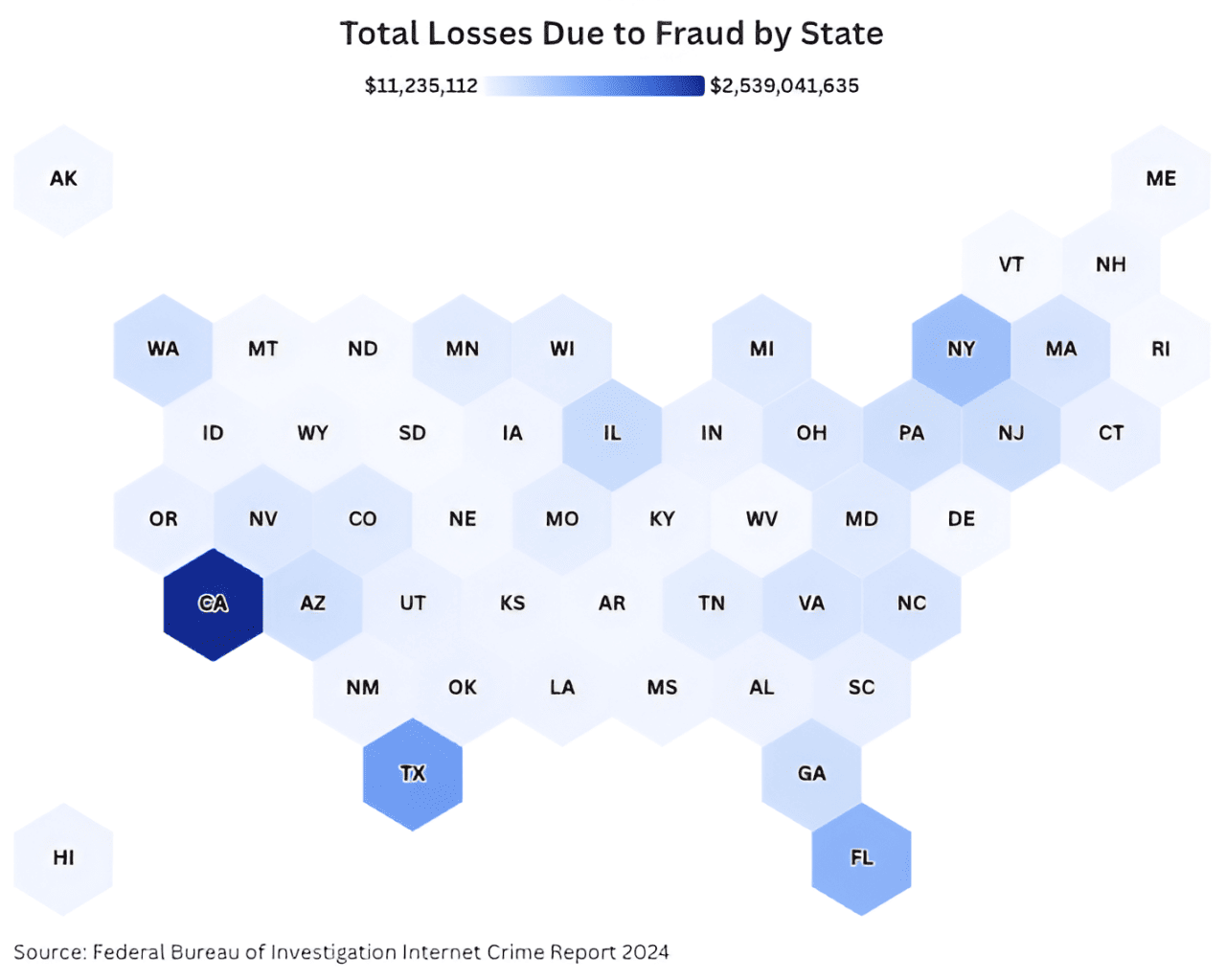

It’s one thing to understand the number of complaints issued but another to see the actual monetary impact. Here is an identical heatmap, but this time, total losses in U.S. dollars by state are outlined:

Even states with moderate complaint volumes may fare worse in total losses, comparatively speaking, if the scams are more sophisticated. With just over $11 million, the lowest reported loss among states, the gravity of the issue should be clear. Specifically, AI-enabled voice impersonation, fake investment platforms, and crypto scams can rapidly drain wallets in states with less sophisticated economies.

Several recurring themes help explain why some states are scam hot spots, and understanding the demographics of each state provides clues to the types of scams they’re likely to experience. Generally, wealth concentrations and a plethora of investment interests are drivers for scams. Areas where residents have higher investable assets will become enticing targets for scammers who are promoting “get-rich-quick” schemes.

The way states regulate nonbank financial services, crypto platforms, or consumer fraud issues varies widely throughout the country and affects how each state detects and deters crime. Increased vulnerabilities lie at the intersection of digital exposure, wealth exposure, and demographic risk factors.

Avoiding falling victim to a scam as a resident of any state, not just those seeing increased targeting, remains as simple as following these tips:

From a policy perspective, finding solutions is a complex proposition. Based on a survey of nearly 10,000 respondents by the Pew Research Center, nearly 7 in 10 (68%) U.S. adults reported that they believed the federal government was doing a poor job of reducing the number of online scams and attacks in the country. Increasing public education campaigns targeting older adults, individuals who have recently moved to a new state, and high-wealth households can be effective in changing this result.

Additionally, policymakers should mandate transparency and regulation for investment platforms and crypto-related assets, especially those that operate across state borders. Facilitating real-time data sharing between states and federal agencies in order to identify emerging scam zones can be beneficial.

Scams in the U.S. are no longer isolated or localized events but dynamic, nationwide operations empowered by AI. Total complaint volumes across the country tell a staggering story, and the geographic distribution across states reveals clear concentration risks among certain areas. Nowhere is immune to scams, but higher-risk states have a confluence of digital access, demographic vulnerability, and high-value targets. To combat this threat, states must increase public awareness at the individual level and implement policy responses at both the state and federal levels.

This story was produced by Lifeguard and reviewed and distributed by Stacker.

Reader Comments(0)