The people's voice of reason

The people's voice of reason

Your home is your haven. Beyond that, it’s an asset and investment that should be protected from losses. Having your home insured does more than provide you with a reliable safety buffer for your valuable investment — it also gives you peace of mind and confidence, knowing you’ll get compensation if disaster strikes and unexpected damage occurs.

There are several types of property damage typically covered by insurance. However, in the event of damage to your property, you may be uncertain whether it falls under the category of damage that your insurance covers.

Learning to identify what types of property damage your insurance covers will empower you to respond correctly when issues arise. Performance Adjusting Public Insurance Adjusters compiled this detailed guide to provide you with all the information you need.

Property damage is not something you expect to happen. However, it’s something you should plan for in the event of unforeseen circumstances, whether it’s an accident or a natural disaster out of your control. Homeowners insurance is one way to protect your finances against the potentially devastating effects of property damage.

Let’s examine the standard types of coverage a homeowners insurance policy might include.

Home Structures

Homeowners insurance provides broad protection for your home itself and other structures attached to it, including your porch, deck and garage. It could also cover stand-alone structures on your property, such as a shed or a fence. Depending on the details of your policy, this insurance could cover damage caused by wind, fire, hail and lightning, among other things.

Personal Property

This coverage includes your personal belongings, such as furniture, clothes and jewelry. It’s typical for homeowners insurance policies to cover personal property, whether located inside your house or anywhere else — for instance, if your jewelry is stolen at a party away from your home, it’ll most likely be covered. Some disasters that a homeowners insurance policy will protect your personal property against include fire, storm and water damage.

Liability Coverage

Homeowners insurance offers coverage for bodily injuries or damage to the property of others caused by you, or any member of your household, including your pets. There are strict provisions that guide liability coverage. For example, while your policy may cover dog bites to other people, it won’t cover intentional acts to harm others.

Additional Living Expenses

Severe damage to your home may render it temporarily uninhabitable, resulting in increased costs for alternative accommodations. In such a case, homeowners insurance will cover extra expenses you incur living away from home, pending when your home is rebuilt. However, some insurance policies limit the time frame for this coverage.

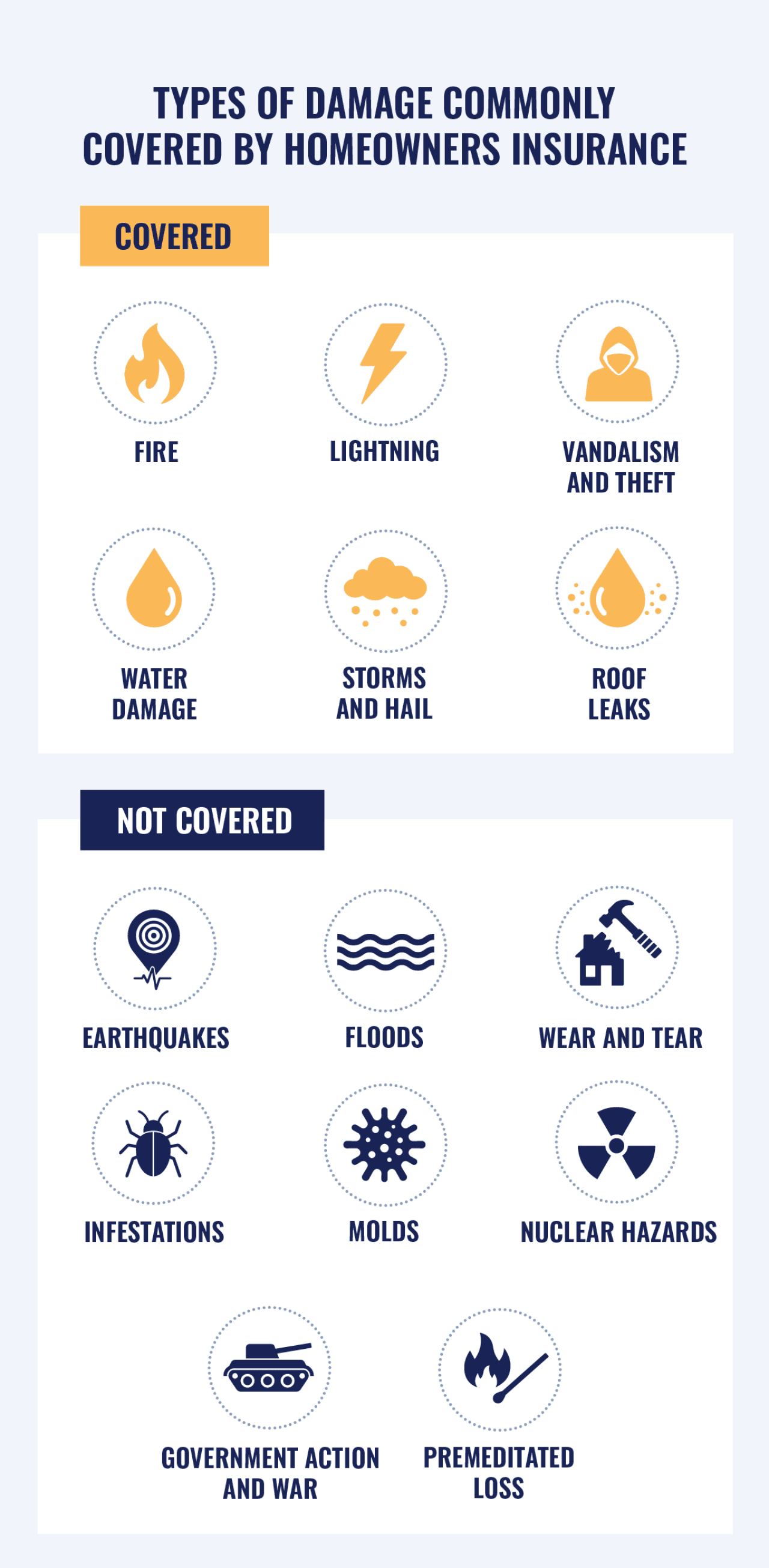

The types of damaging events or perils covered in a homeowners insurance policy are not set in stone. However, you can expect each provider to cover some common types of damage. These include:

While you can expect most homeowners insurance policies to cover specific perils, some types of perils are usually not covered. These include:

If specific types of property damage aren’t included in your policy’s covered perils and you want coverage for them, you can obtain a policy endorsement. A policy endorsement is a written amendment that allows you to change, add or restrict the coverage terms of a standard insurance policy. For instance, if you want coverage for property damage caused by infestation, you can obtain a policy endorsement to cover it.

Some common policy endorsements you can explore are:

Insurance companies offer varying coverages for different types of perils. To know for sure what your particular homeowners insurance policy covers, follow the steps below.

Obtaining a homeowners insurance policy is the first, but not the only, step in securing your home investment. It’s crucial to examine and review the details of your specific policy. Some important details to note when reviewing your policy are:

If the damage to your property is not included in the covered perils section, the next step is to review the policy endorsements section. This step will determine if you purchased additional protection for specific risks not included in the base policy.

Whether they’re included in the covered perils section of your insurance policy, some specific types of property damage require consideration of the nature of the damage. Most insurance policies will only cover damage that is sudden, unexpected or accidental.

For instance, some homeowners insurance policies will cover property damage resulting from mold caused by an abrupt dehumidifier failure. On the other hand, if the mold results from neglect or inadequate maintenance, most policies typically will not cover any damage it causes.

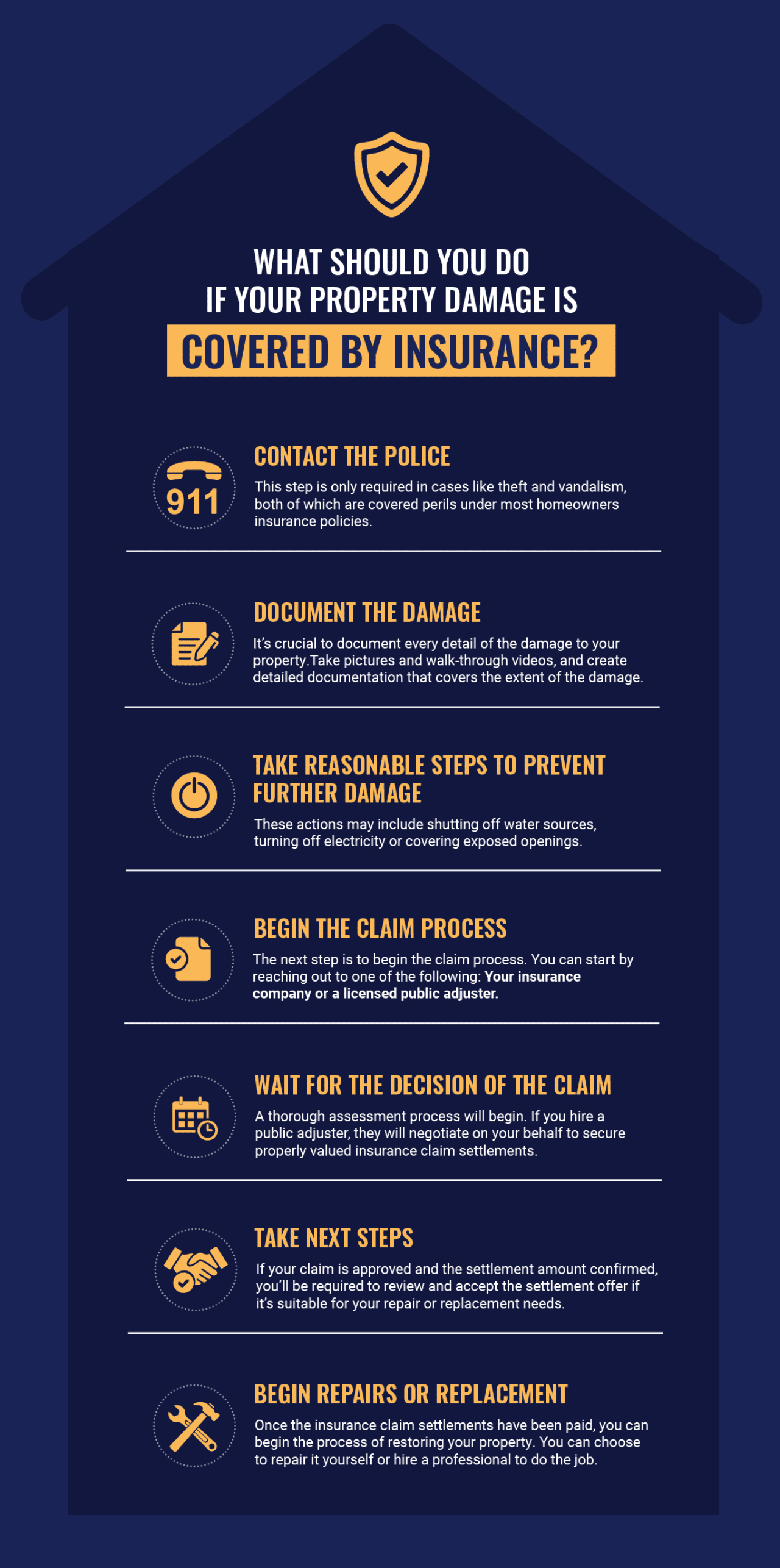

If you’ve experienced property damage that is covered by your homeowners insurance policy, you’ll need to take several steps to set things in motion.

Contact the Police

This step is only required in cases like theft and vandalism, both of which are covered perils under most homeowners insurance policies. Promptly alerting the police and filing the necessary reports in such cases can significantly improve your claim. Conversely, delaying or failing to report altogether can result in the case getting denied.

Document the Damage

It’s crucial to document every detail of the damage to your property, whether it’s caused by vandalism, fire, storm or any other disaster. Documenting the damage helps provide proof to support and expedite your claim. Take pictures and walk-through videos, and create detailed documentation that covers the extent of the damage.

Take Reasonable Steps to Prevent Further Damage

Where it’s safe, you should take reasonable actions to prevent the damage from worsening. These actions may include shutting off water sources, turning off electricity or covering exposed openings. Most insurance policies highlight this step as your duty to mitigate, an obligation required to minimize additional loss or deterioration after the initial incident. Failing to carry out this obligation may weaken your claim.

Begin the Claim Process

Once you have adequately documented the damage, the next step is to begin the claim process. You can start by reaching out to one of the following:

Wait for the Decision of the Claim

After you’ve initiated the claim, a thorough assessment process will begin. If you hire a public adjuster, they will negotiate on your behalf to secure properly valued insurance claim settlements. When a decision is reached regarding your claim, the insurer will notify you.

Take Next Steps

The insurance company’s decision about your claim will determine the next steps you’ll take. If your claim is approved and the settlement amount confirmed, you’ll be required to review and accept the settlement offer if it’s suitable for your repair or replacement needs. You are also allowed to negotiate or dispute the settlement offer if it underestimates the actual cost of the damage or loss.

Your insurance claim may be denied for several reasons, including a lack of evidence or inaccurate application information. If this happens, you can explore several options, including mediation and arbitration, formal appeal and legal action. Unfortunately, at this point, it may be too late to seek the help of a public adjuster if you didn’t already have one — many public insurance adjusters steer clear of already denied insurance claims.

Begin Repairs or Replacement

Once the insurance claim settlements have been paid, you can begin the process of restoring your property. Depending on the nature of the damage, you can choose to repair it yourself or hire a professional to do the job.

Your home is a valuable asset, and as such, you should take every possible step to protect your investment. Insurance coverage for your property can vary depending on several factors, including the type of policy, the cause of the damage and any exclusions that may apply. Understanding your property damage coverage helps you know what losses are protected and allows you to make informed decisions when filing a claim.

This story was produced by Performance Adjusting and reviewed and distributed by Stacker.

Reader Comments(0)