The people's voice of reason

The people's voice of reason

Lowering healthcare costs and getting clear answers are top priorities. While both a health savings account (HSA) and a health reimbursement arrangement (HRA) offer tax advantages, they operate very differently. Selecting the right option can save you thousands annually in taxes, premiums, and out-of-pocket expenses. To find the answer, you need to understand the difference between an HSA and an HRA.

This comprehensive guide from The Difference Card explains how an HSA and an HRA impact your finances, savings, and long-term security.

In 2025, the average single deductible for employer-sponsored health plans exceeded $1,886, up just over $100 from the previous year. How you fund these costs matters, and choosing the right way to fund starts with these key takeaways:

An HSA is a personal health savings account that works like a bank account for medical expenses. You own and control it, and the funds stay with you even when you leave your job.

To open and contribute to an HSA, you must enroll in a qualified high-deductible health plan (HDHP). The IRS sets strict eligibility and contribution rules each year. Here's how it works:

An HSA is more than a spending account. It can serve as a long-term investment vehicle. After age 65, you can withdraw funds for nonmedical expenses without a penalty. You pay ordinary income tax, similar to a 401(k), and withdrawals for qualified medical expenses are tax-free at any age.

An HSA offers three distinct tax benefits:

This unique triple tax advantage can reduce federal, state, and FICA taxes for many households.

To contribute to an HSA, you must meet these criteria:

The IRS defines an HDHP as a plan with a minimum deductible of $1,650 for self-only coverage and $3,300 for family coverage. Your out-of-pocket maximums can't exceed $8,300 for self-only and $16,600 for family coverage.

The IRS set these HSA contribution limits for 2026 — these limits include both employer and employee contributions combined:

If you maximize contributions annually and invest consistently, an HSA can act as your 401(k) for healthcare. After age 65, you can withdraw funds for nonmedical expenses without penalty, though you will pay income tax. Fidelity reported that a 65-year-old couple retiring today may need over $345,000 for healthcare costs in retirement. An HSA can help you prepare for this.

An HRA is an employer-funded reimbursement arrangement. It's not a bank account you own, but rather a promise from your employer to reimburse eligible medical expenses. You can't contribute your own money to a traditional HRA — only the employer funds it. This means the employer decides:

When you have an eligible expense, you submit documentation and your employer reimburses you, tax-free.

There are several forms of HRA, each serving a specific strategy:

Employers use an HRA to control plan costs by shifting all risk to employees. The HRA allows employers to:

The HRA also increases plan flexibility, allowing employers to design incentives that encourage cost-conscious healthcare use. In 2025, employers continued to face medical trend rates between 6.7% and 7.7% annually. An HRA offers a structured way to manage these increases.

In most cases, your HRA funds stay with your employer after you leave. The employer owns the arrangement, so unused funds typically revert back to them. Some retiree HRA programs allow continued access after separation, but this depends on the plan's design.

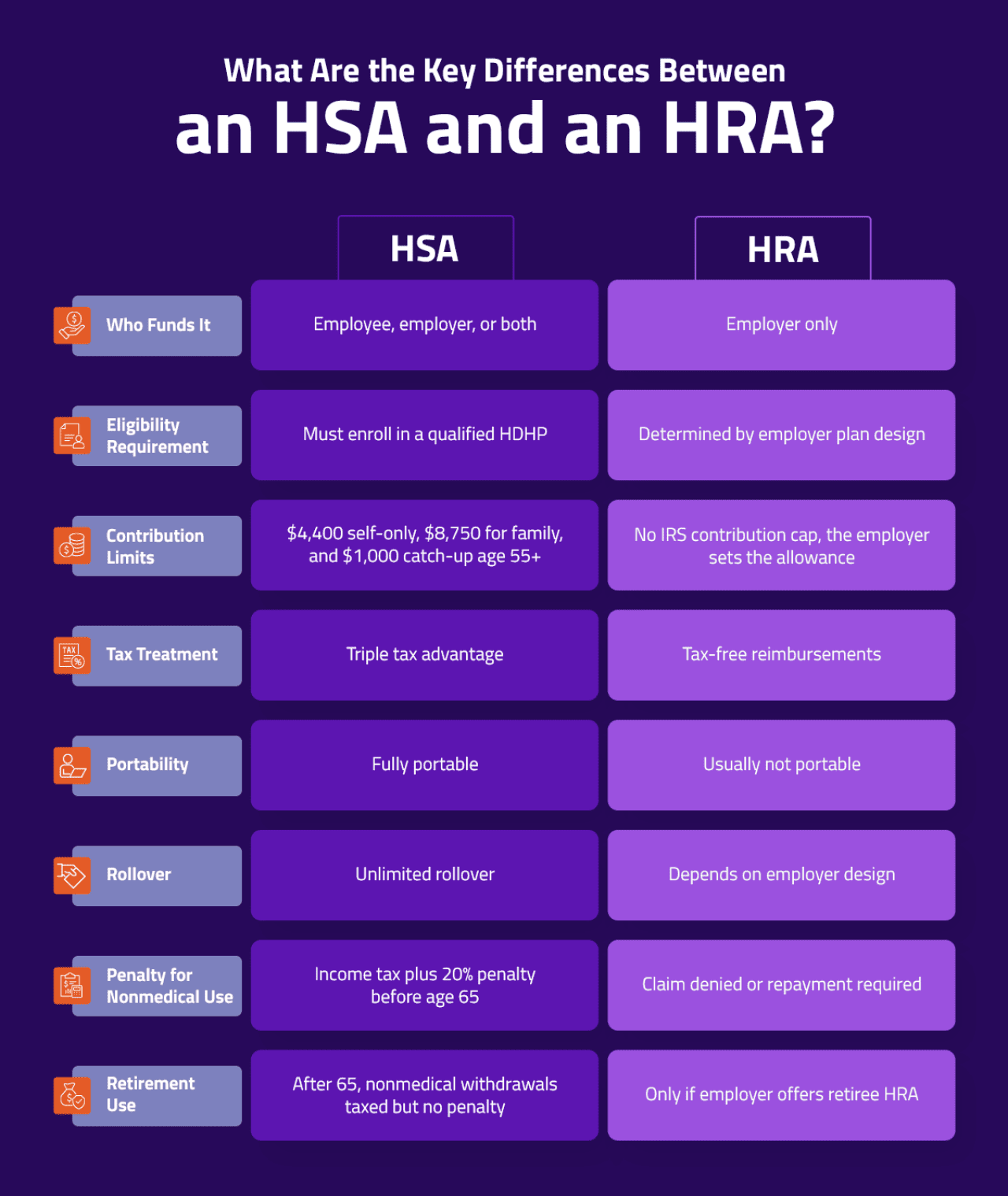

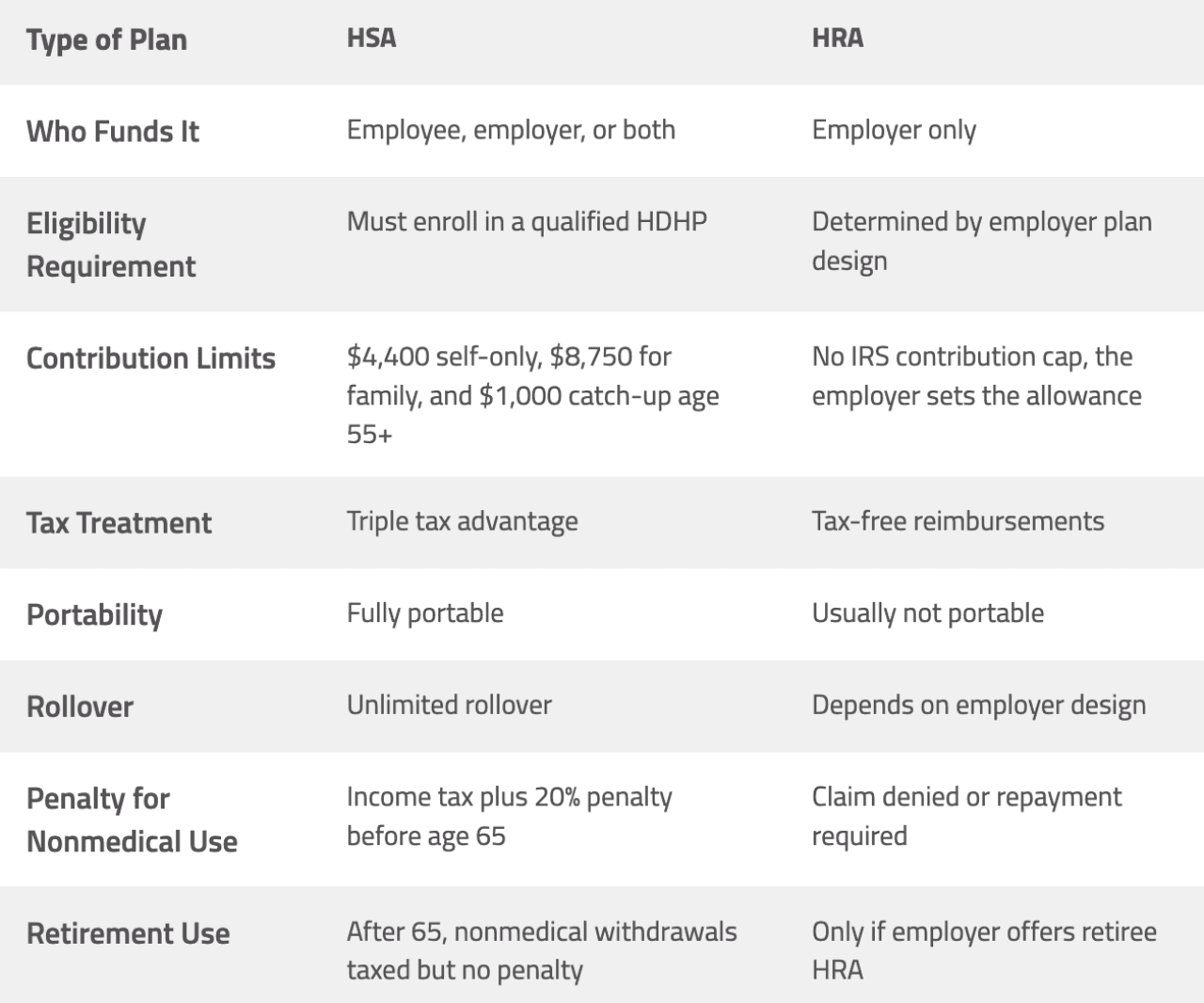

Ownership is the defining difference between an HSA and an HRA.

At a basic level, an HSA is employee-owned and portable. An HRA is employer-owned and reimburses expenses, but it's the details that determine whether you can contribute to, invest in, or combine these accounts.

Understanding specialized HRA designs is critical if you want to stay HSA-eligible:

This table shows the clear distinction, including how an HSA supports long-term savings and an HRA focuses on short-term predictability:

Both HSA and HRA rely on IRS Section 213(d) to define eligible medical expenses. This section covers costs for disease diagnosis, treatment, mitigation, or prevention. Common eligible expenses include:

Many people overlook other eligible categories, which may include:

Cosmetic procedures generally aren't eligible unless they're medically necessary.

With an HSA, if you use funds for nonmedical costs before age 65, nonmedical withdrawals trigger income tax plus a 20% penalty. After age 65, you only pay income tax. With an HRA, nonqualified expenses aren't reimbursed, and improper reimbursements can create taxable income or compliance risks for employers.

One size does not fit all with healthcare. The right answer depends on your health needs, cash flow, and long-term strategy. You should factor in the total cost of care, including deductibles. This means considering that:

In simpler terms, are you focused on saving, or do you expect to use your medical savings much more?

If you rarely visit the doctor and want to build long-term savings, an HSA paired with a qualified HDHP may offer the most benefit. With this strategy, you can lower taxable income, invest unused balances, and accumulate funds for retirement health costs. Over time, compounded growth can offset future premiums and Medicare expenses.

A healthy saver who contributes the maximum to the family annually and earns moderate investment returns can accumulate a sizable amount in their HSA over a decade.

If you expect frequent medical visits, high prescription costs, or ongoing treatment, an HRA-funded plan can give you more predictable support. It can offset high deductibles, reduce immediate out-of-pocket exposure, and stabilize cash flow during high-cost years. For families managing chronic conditions, structured employer reimbursement often delivers stronger year-to-year value.

High utilizers often value stable copays and first-dollar coverage over a long-term tax strategy.

Yes, you can have both, but only if the HRA is HSA-compatible. The IRS restricts HSA contributions if you have disqualifying coverage, so you are looking at an HRA with an HDHP, which is generally structured in one of these ways:

Each structure avoids interfering with HSA eligibility because it does not offer first-dollar medical coverage under the IRS deductible threshold. You generally can't contribute to an HSA if you are covered by a general-purpose HRA that reimburses first-dollar medical expenses. This means that coordination is essential. Misalignment can trigger IRS compliance issues.

You cannot contribute to an HSA if:

In these cases, even partial-month disqualification can reduce your annual HSA contribution limit.

Improper coordination creates compliance risk. Excess HSA contributions trigger IRS penalties until you correct them. Employers must structure an HRA carefully to avoid unintended consequences.

Strategic integration gives you the long-term tax benefits of an HSA while you use an HRA to manage specific costs. This approach supports both healthy savers and high utilizers while keeping you compliant. When designed correctly, the combination will strengthen your financial outcomes and offer your employer better cost predictability. Precision in plan design determines success.

A medical expense reimbursement plan (MERP) is a structured employer reimbursement strategy that often resembles an HRA but can operate alongside a level-funded or self-funded health plan. A MERP reimburses specific costs, such as a corridor deductible. It creates blended funding that reduces premium equivalents while protecting you from high out-of-pocket exposure.

Healthcare financing is complex, with rising premiums, increased deductibles, and regulatory shifts that require disciplined planning. When you understand the difference between health savings plans, you move from confusion to control.

With an HSA, you control the account and decide when to spend or invest. The balance rolls over every year, staying with you through job changes and into retirement. With an HRA or a MERP, your employer controls the structure and funding, providing short-term support but limited portability. This distinction shapes behavior, savings rates, retirement planning, and workforce satisfaction.

The right partner is critical to choosing the right plan. A service provider helps you evaluate plan performance with real data, examining corridor deductibles, aggregate exposure, stop-loss integration, and reimbursement patterns. The result is a recommendation that aligns with your needs, reduces costs, and keeps you compliant.

This story was produced by The Difference Card and reviewed and distributed by Stacker.

Reader Comments(0)