The people's voice of reason

The people's voice of reason

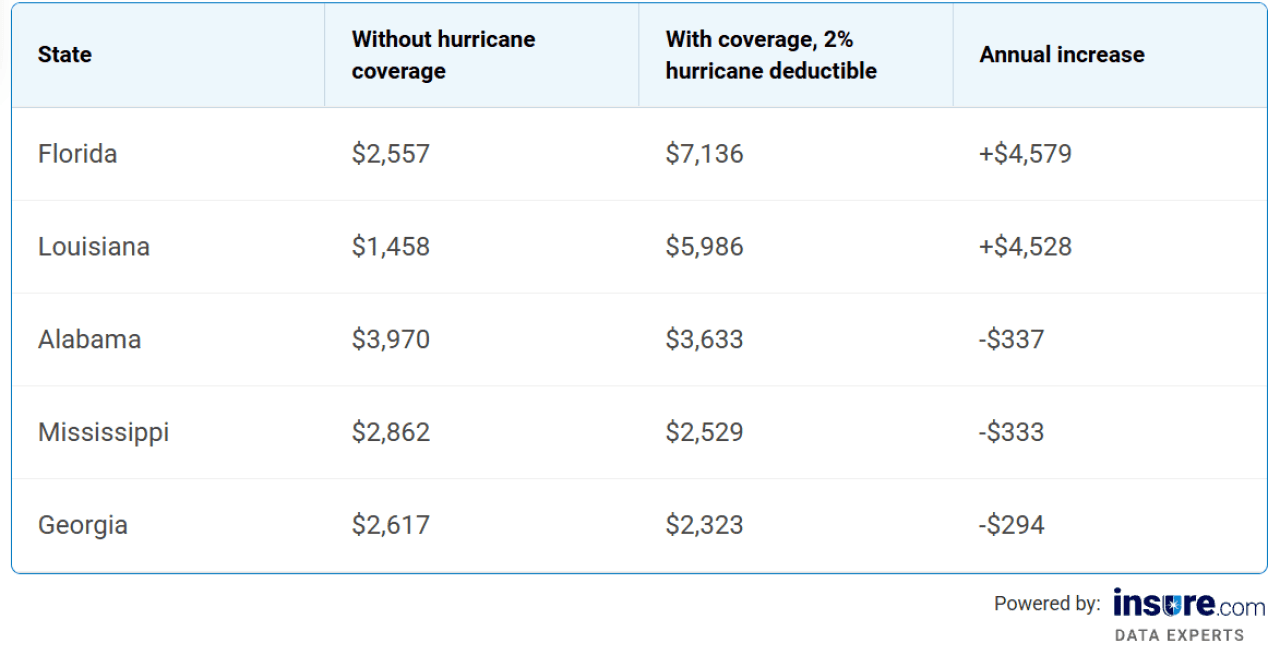

Hurricane coverage adds an average of over $4,500 per year to homeowners insurance premiums in Florida and Louisiana. In Florida, the average premium jumps from $2,557 without hurricane coverage to $7,136 with a 2% hurricane deductible — a difference of $4,579 annually. Louisiana homeowners pay an extra $4,528 per year for the same protection.

This "hurricane tax" reflects the real cost of insuring a home against named-storm damage in the country's highest-risk states. As warmer ocean waters fuel more intense storms and major insurers continue to exit coastal markets, homeowners in hurricane-prone states are paying more — and getting fewer choices — than ever before.

Whether you're a snowbird eyeing a second home in the Sunshine State or a longtime coastal resident reviewing your policy, this guide from Insure.com will help you understand how hurricane deductibles work, when they kick in, and how to lower your premium can save you thousands per year.

A hurricane deductible is a separate deductible that applies when damage is caused by a named storm or hurricane recognized by an official source, such as the National Weather Service.

Nineteen states have hurricane or named storm deductible provisions in place, according to the National Association of Insurance Commissioners. First introduced after the catastrophic losses of Hurricane Andrew in 1992, the adoption of these deductibles expanded after Hurricane Katrina in 2005.

After a major hurricane, people are dealing with a lot of total losses, according to Chris Bacon, chief operating officer of Openly, which provides home insurance in 24 states. “You’re not dealing with houses that are moderately damaged,” Bacon says.

Those losses mean billions are paid out by insurers — $65 billion after Katrina, for instance — and hurricane deductibles were implemented to offset these losses. They’re intended to keep coverage affordable and accessible to homeowners, and there’s no sign they’ll be going away.

“Insurers have generally been raising hurricane deductibles over the last few years,” according to Jasper Cooper, vice president and senior credit officer with Moody’s Ratings.

Climate change is driving homeowners insurance rates higher by intensifying the storms, floods, and wildfires that insurers have to pay for. Across the country, homeowners insurance premiums rose 24% between 2021 and 2024 — twice the rate of inflation — according to a 2025 report from the Consumer Federation of America. With the last 11 years ranking as the warmest on record, according to the World Meteorological Organization, the trend is accelerating, not slowing down.

Climate change is putting more homes at risk of extreme weather and affecting home insurance rates in the following ways:

New pricing technology means insurers can reward individual risk reduction — not just lump you in with the whole neighborhood. Hurricane mitigation features that may lower your premium include:

“You are seeing more carriers that are being more sophisticated,” Bacon says. The more sophisticated the pricing models are, he notes, the more accurately the carriers can price the risk.

That means insurers can set premiums that better reflect the chances of your home sustaining damage. If your home has been hardened to withstand a hurricane, ask your insurer for a wind mitigation inspection to see if you qualify for discounts.

In some parts of coastal states like Florida, Louisiana, and Texas, hurricane damage isn't covered by a standard homeowners policy, though coverage depends on where you live — in lower-risk parts of the same state, hurricane damage may already be included. To get that protection, homeowners have to add the coverage with a separate hurricane deductible — usually 2% of their home's insured value — which significantly raises their annual premium. The numbers below reflect average premiums with that 2% hurricane deductible added, since that's the realistic cost of being covered for hurricane damage in these states.

Florida homeowners pay more than anyone else in the country. With a 2% hurricane deductible, the average Florida premium is $7,136 a year — more than ten times what a homeowner in Hawaii pays ($659), where hurricane damage isn’t covered at all. These figures are based on a standard policy with $300,000 in dwelling coverage, $300,000 in liability coverage, and a $1,000 all-perils deductible.

In states where hurricane damage is excluded from a standard policy, adding hurricane coverage can dramatically increase your annual premium.

According to our data, Florida and Louisiana show the clearest "hurricane tax" pattern — premiums jump by roughly $4,500 a year with hurricane coverage and a 2% deductible. In other coastal states like Alabama, Mississippi, and Georgia, premiums actually decrease slightly when a 2% hurricane deductible is added, because hurricane damage is included in a standard policy in those states, and the higher deductible just shifts more risk onto the homeowner.

The table below shows the full picture across these states.

Most of the states with hurricane or named-storm deductibles are coastal states along the Gulf or Atlantic, but a few, like Pennsylvania, sit further inland — they're included because hurricanes can travel well past the coast.

States with hurricane or named-storm deductibles:

States outside this list either don't face meaningful hurricane risk or already cover hurricane damage under their standard windstorm-and-hail coverage. Inland states like Kansas, Oklahoma, and Colorado see hail and tornado damage rather than named storms, and they typically have their own separate wind and hail or windstorm deductibles to handle those risks.

States in the Mountain West and Pacific Northwest face wildfire and earthquake risks instead, which carry their own coverage rules. Hurricane deductibles only show up where hurricane risk is significant enough to justify a separate, higher deductible — and where state regulators have approved their use.

A hurricane deductible only applies when the National Weather Service or National Hurricane Center officially classifies a storm as a hurricane — meaning sustained winds of 74 mph or more. A named-storm deductible covers a broader category: it applies to any storm the NWS has named, including tropical storms (39-plus mph winds), tropical cyclones, and typhoons.

The difference is when the higher deductible kicks in. If a named tropical storm causes $20,000 in roof damage to your home:

A named-storm deductible always covers hurricanes, since hurricanes are by definition named storms. But a hurricane deductible doesn't always cover tropical storms. Which one applies to you depends on your state and your specific policy — check your declarations page for the exact wording.

Whether you can skip the hurricane deductible — and whether you should — depends on where you live. If you live in a hurricane-prone area, hurricane damage is treated as a separate category, with its own deductible. In others, it's just lumped in with regular wind damage, the same as a thunderstorm or a tree falling on your roof.

In states without hurricane deductibles at all (like Kansas, Colorado, Vermont, and most inland and Western states), there's no tradeoff to make. Your homeowners policy uses a single all-perils deductible — typically $1,000 — that applies to every covered loss, including the rare hurricane that travels far enough inland to do damage. Premiums in these states reflect other regional risks like hail, tornadoes, or wildfires, not hurricane exposure.

Whether to skip, lower, or raise your hurricane deductible comes down to three things: how much risk you're carrying personally, whether you have a mortgage, and what your state's rules allow. Use these guidelines as a starting point:

Before making a decision about a hurricane deductible, be sure you understand your state’s rules and your insurer’s policy details.

“There’s a lot of nuance in the policies, and different carriers apply deductibles differently,” Bacon says. Independent insurance brokers can be a valuable resource to help you understand costs and coverage options.

The deductible math can catch homeowners off guard, because it's based on the home's insured value — not the size of the claim. Here's a real-world example:

Imagine a home insured for $400,000 with a 2% hurricane deductible. A named hurricane causes $80,000 in roof and water damage.

If that same home had a standard $1,000 all-perils deductible (because the damage was caused by a regular storm, not a named hurricane), the homeowner would pay $1,000 out of pocket and the insurer would cover $79,000. That's the trade-off: Hurricane deductibles let insurers offer coverage in high-risk areas, but homeowners shoulder a much larger share of the cost when a named storm hits.

The higher the percentage you choose, the larger that out-of-pocket cost gets. A 5% deductible on the same $400,000 home would mean $20,000 out of pocket before insurance pays anything.

Even the best hurricane coverage doesn't pay for flood damage. Flood coverage is a completely separate product, and homeowners have to buy it on their own.

The distinction matters because most hurricane damage is actually water damage. Storm surge pushes ocean water inland, heavy rainfall floods streets and basements, and rivers overflow their banks days after the wind has died down. A home that survives the wind intact can still be destroyed by the water that follows — and without flood insurance, the homeowner pays for those repairs themselves.

Hurricane coverage handles wind damage. Flood insurance handles water damage from rising water. The two work together, and most coastal homeowners need both.

Most flood insurance in the U.S. is sold through the National Flood Insurance Program (NFIP), administered by FEMA. A handful of private insurers also sell flood coverage, sometimes with higher limits than NFIP. A few things to know:

Use FEMA's Flood Map Service Center to look up your home's flood zone in 30 seconds. If you're in a "Zone A" or "Zone V" area, you're in a high-risk zone and should already have flood insurance — your mortgage lender probably requires it. If you're in "Zone X," you're in a lower-risk area, but coverage may still be worth it. The 30-day waiting period means now is the time to buy, not after a storm forms.

You can save money on hurricane insurance by taking proactive steps to minimize storm damage and by regularly looking for new coverage. Try these steps to reduce your home insurance premiums:

The trigger varies by state and insurer, but most policies use one of three:

The trigger language matters because it determines which deductible applies to a claim. A roof damaged by 70-mph winds during a tropical storm might be covered under your standard $1,000 deductible — or it might trigger your 2% hurricane deductible — depending on which trigger your policy uses. The Insurance Information Institute recommends reviewing your declarations page and asking your insurer to walk you through exactly when your hurricane deductible activates, before storm season starts.

What states have hurricane deductibles?

Nineteen states have hurricane deductibles. These are mainly states along the East Coast and Gulf, although insurers in some inland states may offer hurricane deductibles because of storm-track exposure.

How is a hurricane deductible calculated?

Hurricane deductibles are typically a percentage of your home’s insured value and often range from 1% to 10%. Flat rate deductibles are sometimes available. For a home with a $450,000 dwelling coverage limit, a 2% hurricane deductible would require homeowners to pay $9,000 out of pocket before insurance coverage begins.

Is a hurricane deductible the same as a windstorm deductible?

No, a hurricane deductible only applies to damage caused by named storms. Some insurance policies may have windstorm deductibles that apply to damage caused by any wind event.

Why is Florida home insurance so expensive?

High-intensity hurricanes, rising construction costs and a history of claims litigation have all led to increasing home insurance premiums in Florida. Major insurers have also left the state, leading to less competition and higher rates for residents.

Can I negotiate my hurricane deductible?

Not usually, but you can usually choose from available options. For instance, Florida law requires companies to offer hurricane deductibles of $500, 2%, 5% or 10%.

This story was produced by Insure.com and reviewed and distributed by Stacker.

Reader Comments(0)