The people's voice of reason

The people's voice of reason

Mid-May 2026 saw a dramatic intersection of legal reprieve, aggressive threats, and targeted diplomacy defining global commerce. The U.S. executive branch successfully stabilized its immediate economic policy as an appellate court paused a ruling that had briefly neutralized the nation's 10% global surcharge. Empowered by this judicial lifeline, Washington escalated its transactional pressure on Europe by threatening to raise tariffs on European Union automobiles to 25%, citing unmet trade concessions.

However, as Freight Right observed, the week’s most significant breakthrough occurred in Asia, where a high-profile summit culminated in China committing to buy $17 billion annually in U.S. agricultural goods. This massive purchase agreement offers a strategic cushion to American farmers, even as China's overall share in the U.S. import market continues to crater under the weight of a near-37% effective tariff rate.

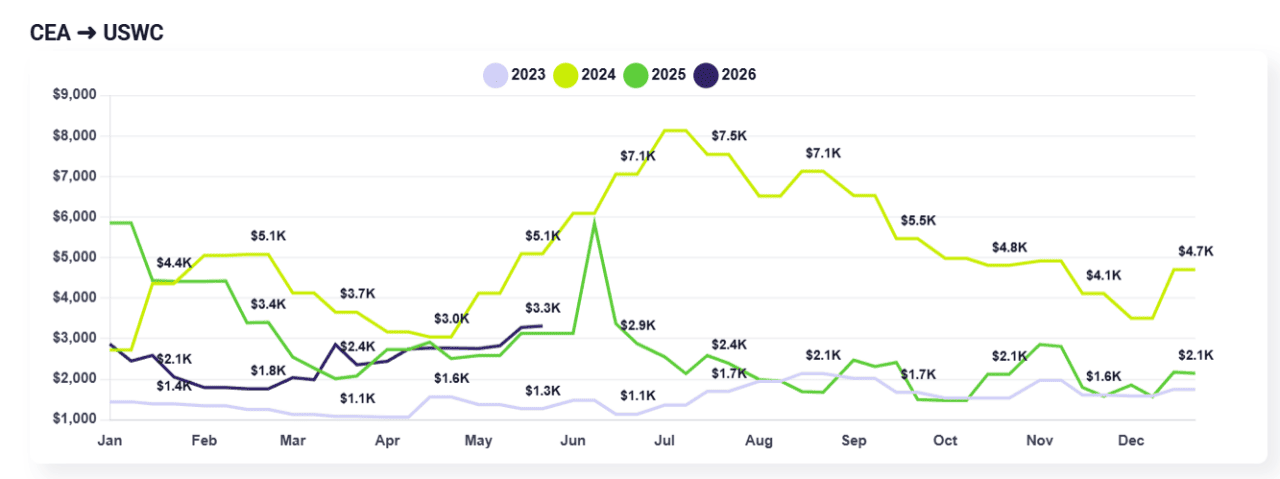

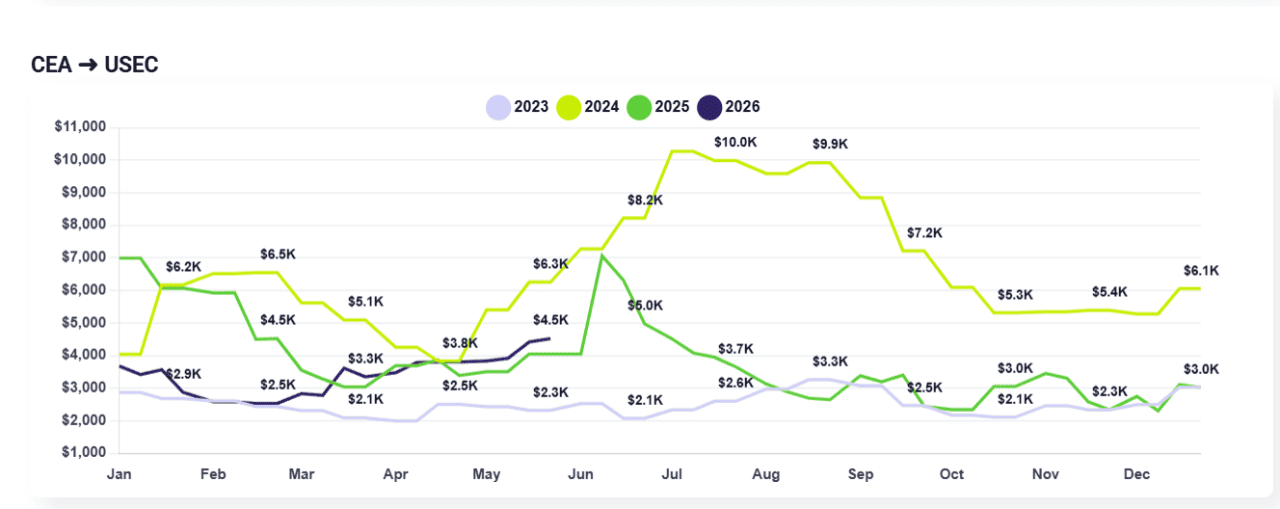

The ocean freight market has experienced sharp week-over-week rate increases across major lanes from China/East Asia (CEA) to North America. Spot rates to both coasts have surged, effectively doubling compared to early March baselines, where pricing sat around $1,600 to $1,700 per container.

CEA to USWC: Rates increased by roughly $500 to $600, bringing the current pricing to $2,800–$3,400 per container.

CEA to USEC: Rates have climbed to $3,700–$4,500 per container.

While a few special agency rates remain scattered across the market, oceanfreight capacity is severely constrained.

Freight Right’s Lowest Rate indicators are finding that importers can find spot rates as low as $2,800 from China to the U.S. West Coast and $3,787 from China to the U.S. East Coast. Talk to your freight forwarder about the options available to you.

The short-term outlook indicates further friction for typical importers. Carriers have already signaled intent to push rates even higher moving into June, a sign that they anticipate capacity restrictions will successfully hold.

If this upward trajectory persists through June, it could fundamentally disrupt the traditional Q3 peak season (July through September). Because shippers are scrambling to pull demand forward right now out of fear of future space shortages, the industry may see a flat or nonexistent peak season later this summer. This would mark the second or third consecutive year where traditional seasonal shipping patterns have dissolved in favor of artificial, carrier-driven market cycles.

A potential demand buffer may arrive in approximately two months as government tax refunds flow back into the market, potentially stimulating consumer spending and easing liquidity constraints for smaller importers. Until then, only enterprise brands with massive negotiating leverage or seasonal shippers with zero scheduling flexibility will maintain consistent volume, leaving the rest of the market sidelined.

This story was produced by Freight Right and reviewed and distributed by Stacker.

Reader Comments(0)