The people's voice of reason

The people's voice of reason

Cash is often crowned king — and for good reason. It typically upholds its value and allows you to instantly make purchases. When you add cash into an account or investment, it's also important to understand how easily you can access it, which is known as liquidity, reports Ally Financial.

Financial liquidity refers to the ease with which an asset — anything ranging from a money market savings account to an ETF to real estate — can be converted into cash relatively quickly.

While several classifications exist (for example, funding liquidity), the main types are:

Everyone's motives for having cash readily available may differ and vary over time. But you'll likely have moments in life where you need cash on hand, whether it's accessible funds for an emergency, the ability to capitalize on timely investment opportunities or even to limit your exposure to market volatility. An asset that cannot be quickly converted into cash without a significant loss of value is considered an illiquid asset. Examples include collectibles and fine art, real estate and collectible luxury items.

You can use several different ratios to assess liquidity:

Market liquidity can be unpredictable and impacted by many factors, including:

Some assets are highly liquid, while others have far less liquidity. The degree of liquidity is often determined by regulations and required processes; for example, a stock can usually be sold more quickly than a real estate transaction due to the required steps, as well as the market and demand.

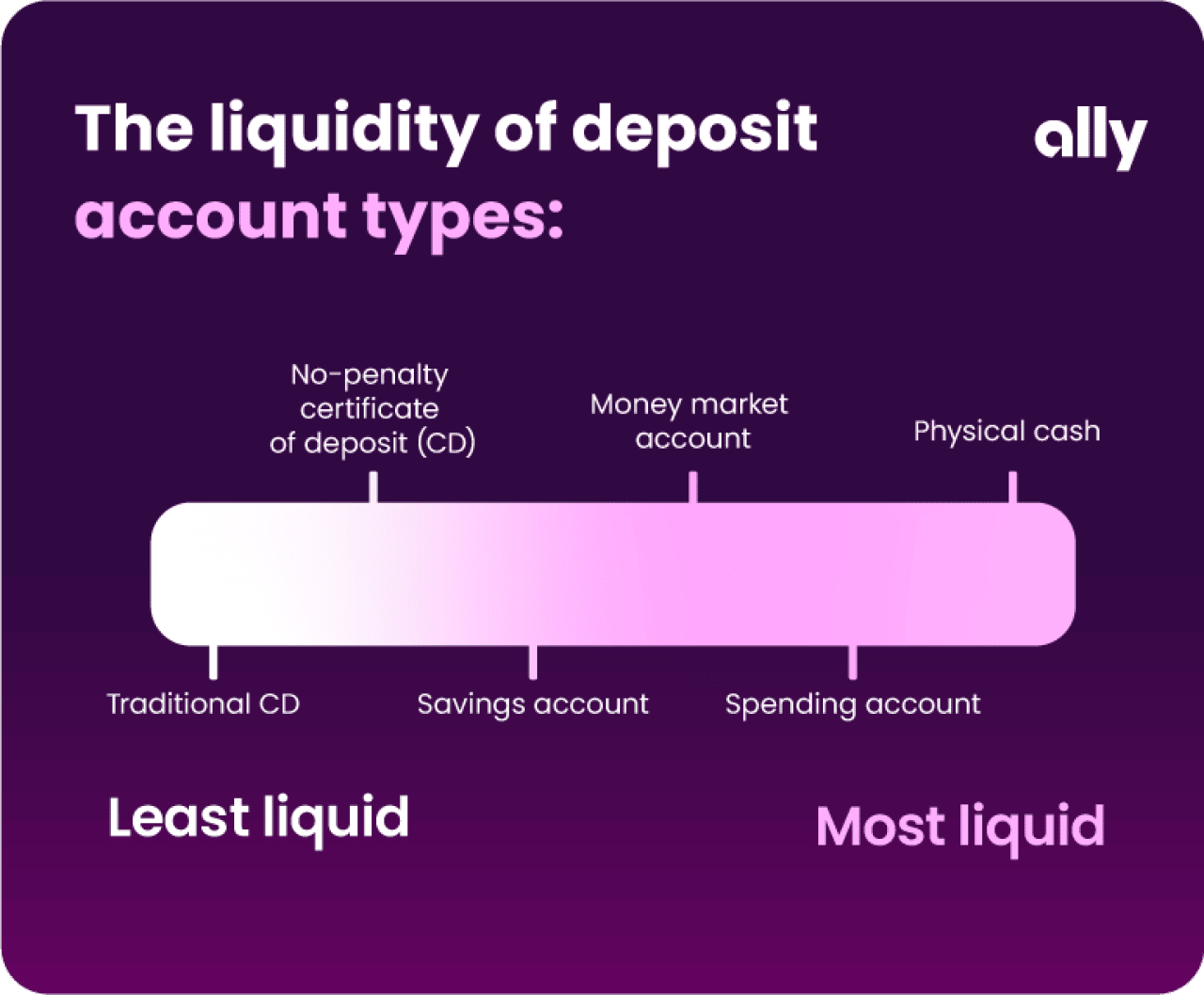

The liquidity of deposit accounts varies by account type. Here’s what to know about each:

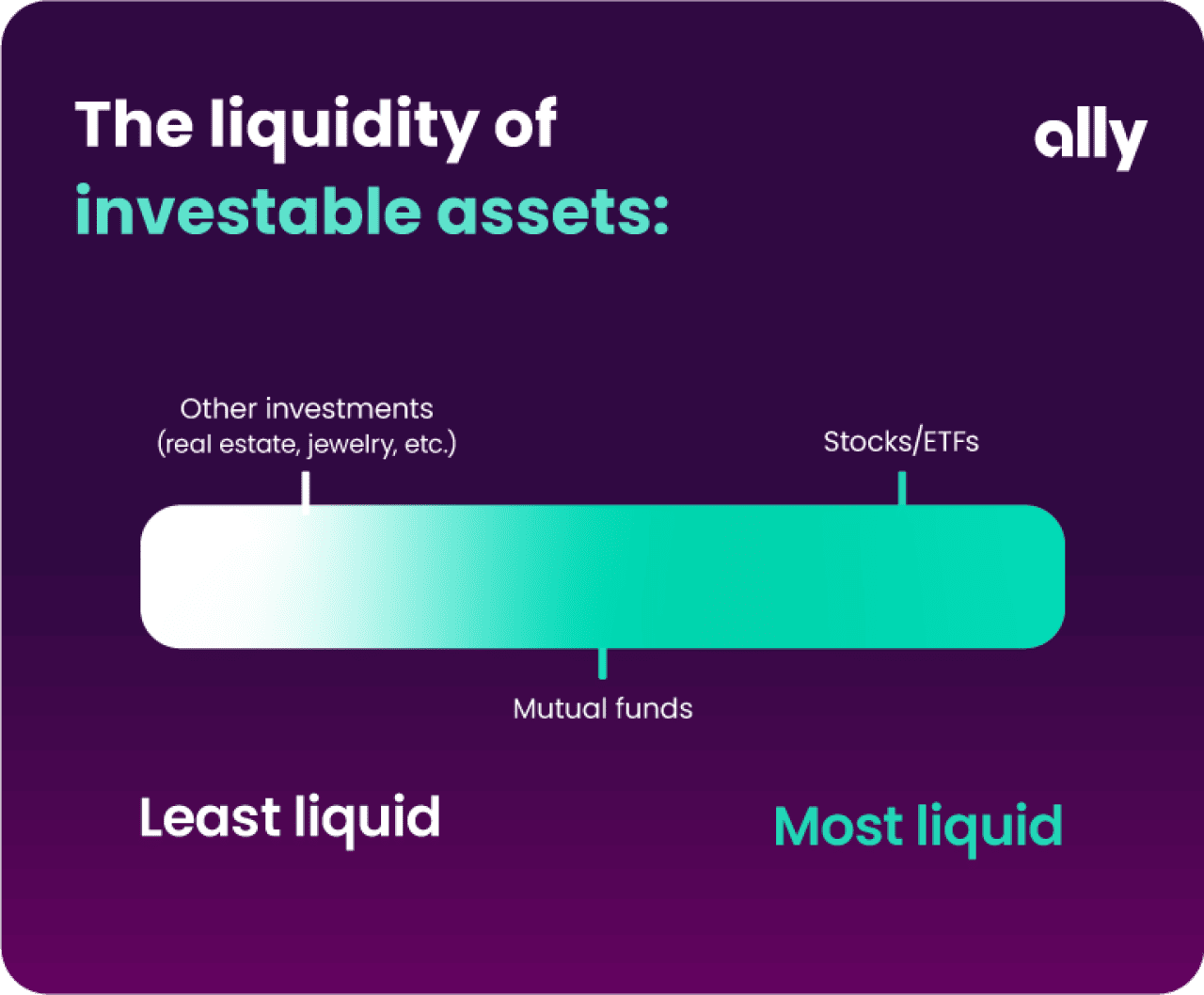

Some investment types are highly liquid, while others have far less liquidity. Keep in mind, the liquidity of stocks and ETFs depends on market activity and investor demand. Large, actively traded securities tend to be more liquid, while those with lower volume can be more illiquid.

Mutual funds do not have intraday liquidity like stocks or ETFs and are only priced once per day.

Other non-security investments are not traded on a public exchange and are typically the least liquid. It can include a business, real estate and even collectible items like art or rare coins. Because it can take several steps to sell these types of investments, extra time is typically needed before you receive any cash in exchange.

Before you invest, you should carefully review and consider the investment objectives, risks, charges, and expenses of any mutual fund or exchange-traded fund (ETF) you are considering. ETF trading prices may not necessarily reflect the net asset value of the underlying securities.

The good news is you have plenty of deposit account types and investment choices to choose from when factoring in liquidity. A good rule of thumb is to diversify your portfolio and always allocate your funds based on your individual preference, risk tolerance and personal goals.

This story was produced by Ally Financial and reviewed and distributed by Stacker.

Reader Comments(0)